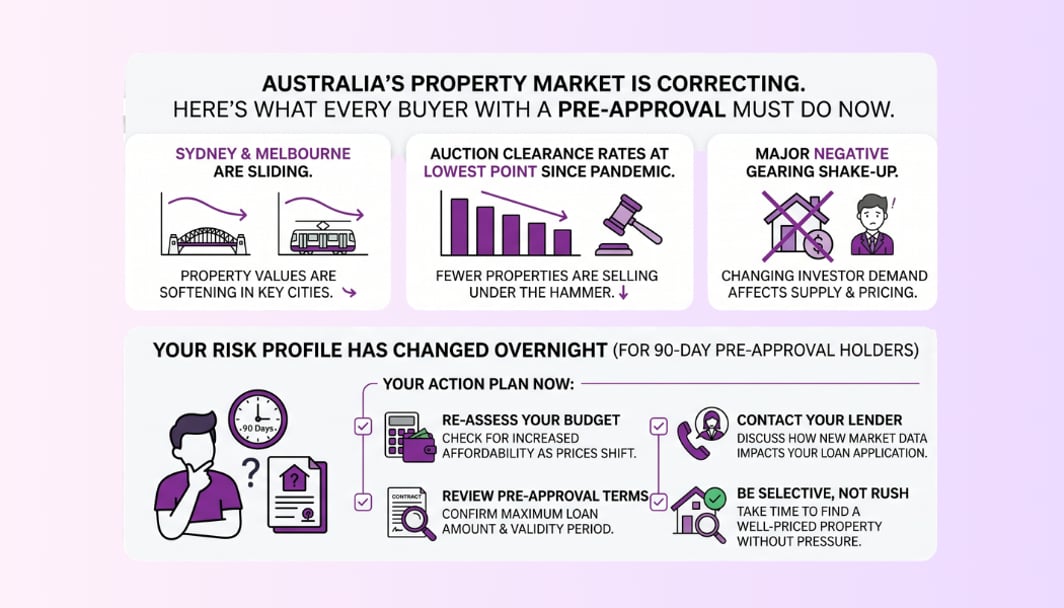

Sydney and Melbourne are sliding. Auction clearance rates just hit their lowest point since the pandemic. A major negative gearing shake-up is pulling investor demand out of the market. If you're holding a 90-day pre-approval, your risk profile has changed overnight.

0.5%

Sydney monthly decline

50.4%

National clearance rate 6-yr low

1.0%

Sydney below late-2025 peak

What the May 2026 data is actually telling us?

A 50.4% clearance rate is not a soft landing, it is a market where roughly half of all sellers are failing to find a buyer. - Pravin Mahajan, Founder of Bheja.ai

For the past two years, buyers navigated a relentless sellers' market defined by tight supply and strong demand driven by record net overseas migration. That environment is now shifting. Property analytics firm Cotality ( formerly CoreLogic) released May 2026 data showing that national home value growth has stalled, and that a meaningful divergence has opened between capital cities and regional markets.

The most telling signal is not a price chart, it is the auction room. National clearance rates have fallen to 50.4%, the lowest reading since May 2020 at the height of the initial pandemic shock. A clearance rate at this level means that for every two properties taken to auction, one fails to sell. That is not a soft landing. That is a market where vendor expectations and buyer willingness to pay have structurally diverged.

The geographic picture is uneven. Sydney home values declined 0.5% in the most recent month and now sit 1.0% below their late-2025 peak. Melbourne recorded a 0.3% monthly decline. Meanwhile, markets in Queensland and Western Australia have remained more resilient, supported by stronger interstate migration and comparatively lower price bases.

Policy headwind

The May 2026 Federal Budget announced significant changes to negative gearing and capital gains tax concessions on established residential properties, effective July 1, 2027. While the changes do not take effect immediately, investor sentiment has deteriorated rapidly.

A layer of demand that previously absorbed a large share of inner-city stock, particularly off-the-plan apartments and investment-grade houses, has materially pulled back. The medium-term impact on prices in investor-heavy suburbs warrants close monitoring.

Two factors that bulls point to deserve honest acknowledgment. First, net overseas migration remains elevated, underpinning long-run housing demand. Second, the Reserve Bank of Australia delivered two consecutive cash rate reductions in early 2026, improving borrowing capacity across the board. A case exists that these factors will put a floor under prices. The honest assessment, however, is that neither force has been strong enough to prevent the current decline in the Southeastern capitals, and that the full effect of the negative gearing changes on investor participation remains unknown.

The Negative Equity Trap: A plain-english explanation

When a market transitions from growth to correction, the primary risk for a buyer using maximum leverage is not the abstract idea of falling prices, it is a specific mechanical trap called negative equity. Understanding precisely how it happens is the first step to avoiding it.

Consider a property purchased at $1,000,000 with a 5% deposit of $50,000. The mortgage sits at $950,000, giving you a Loan-to-Value Ratio (LVR) of 95%. Your ownership stake, your equity, is that $50,000.

Now assume the local market undergoes a modest 5% structural correction. The bank's independent valuation of the property falls to $950,000. Your equity is now zero. If values decline a further 3%, you owe more to the bank than the property is worth. You are in negative equity.

Negative equity does not automatically trigger foreclosure, our repayments continue as normal and daily life is largely unaffected. But it quietly destroys your financial flexibility. You cannot refinance to a cheaper interest rate, because no lender will accept you at above 100% LVR. You cannot sell without covering the shortfall in cash. You are, in practical terms, locked in until values recover. In a prolonged correction, that wait can span years.

Key definition

LVR (Loan-to-Value Ratio) is the size of your mortgage as a percentage of the property's current bank valuation, not what you paid for it. Lenders typically require an LVR below 80% to refinance without Lenders Mortgage Insurance (LMI). Above 95% LVR, most lender panels will not extend new credit.

Four Practical Steps to Protect Your Capital Right Now

The appropriate response to a correcting market is neither panic nor complacency. Do not let your pre-approval lapse, a good rate lock and borrowing assessment are worth preserving. Instead, adjust your bidding strategy from maximum stretch to defensive positioning. Here is how.

- Apply a 5–7% bidding buffer: Calculate your maximum pre-approved limit, then subtract 5% to 7% and treat the resulting number as your unconditional walk-away price. This buffer absorbs a potential valuation shortfall and keeps your LVR in a safer zone. It also gives you room to negotiate without emotionally overstretching at auction.

- Track days on market for your target suburbs: Total listings are currently running approximately 5% above the five-year seasonal average, according to Cotality data. When properties in your target suburb sit on the market beyond 35 days, it signals that vendors have not yet accepted new price realities. In this environment, lowball initial offers are not insulting, they are rational. Time is on the buyer's side.

- Commission an independent valuation before you bid: Before making an unconditional offer or bidding at auction, ask your mortgage broker to order an Automated Valuation Model (AVM) report. This is a bank-logic assessment of what the property is worth today, distinct from the agent's price guide, which may reflect peak-market comparable sales. If the AVM comes in materially below the guide price, treat that as a hard ceiling for your bid.

- Review your LMI position and exit strategy before you sign: If you are purchasing with below 20% deposit, Lenders Mortgage Insurance premiums can add tens of thousands of dollars to your cost. In a correcting market, that expense becomes even harder to recover. If you can extend settlement timing to allow additional savings, or negotiate a vendor deposit contribution, do so. Your broker can model the exact LMI cost at different deposit levels.

The contrarian case: why waiting also has risk

A correction is not a crash, and holding out indefinitely carries its own risk. If the RBA delivers further rate cuts later in 2026, borrowing capacity will increase, and competition will return quickly in undersupplied markets. The goal is not to time the bottom; it is to buy at a price that leaves you with meaningful equity in a range of market scenarios. Defensive positioning achieves that. Paralysis does not.

Navigating a correcting market

Know your real LVR before you bid

Bheja.ai tracks automated property valuations across Australian postcodes daily, stress-tests your borrowing capacity against current lender panels, and alerts you when your equity position changes. Built for buyers who want data, not hype.

Sources & methodology

Cotality (formerly CoreLogic) National Home Value Index, May 2026 release. Monthly and peak-to-current change figures for Sydney and Melbourne.

Cotality Auction Market Preview, week ending May 25, 2026. National preliminary clearance rate: 50.4%.

Australian Federal Budget 2026–27, Budget Paper No. 2. Negative gearing limitation on established residential properties; capital gains tax discount changes. Effective date: July 1, 2027.

Cotality Total Listings data, May 2026. Capital city stock levels vs. five-year rolling average.