Why buying a home feels harder than ever

The rising cost of living has become one of the defining financial stories of recent years. Groceries cost more than they used to. Petrol, electricity and insurance have all become more expensive, increasing pressure on household budgets across Australia.

Yet rising everyday expenses don't fully explain why buying a home feels harder than it did fifteen years ago.

The bigger story is what happened to house prices, interest rates and borrowing capacity. Together, these forces have changed what Australians can afford to buy, how much banks are willing to lend and how accessible home ownership has become.

The difference becomes clearer when these changes are compared side by side.

Between 2010 and early 2026, a simple weekly basket of bread, butter and eggs roughly doubled in cost, rising by around 10 dollars per week based on CPI food price trends and supermarket data. Over the same period, the mean Australian dwelling increased in value by more than $660,000.

*Based on early ABS estimates of the total value of the dwelling stock and long‑run residential property price series

**ABS Mean Residential Dwelling Price, March Quarter 2026.

Both are examples of rising prices, but they influence household finances in very different ways.

An additional $10 a week at the supermarket affects this week's household budget. An additional $660,000 on the price of a home affects the size of the deposit required, the amount borrowed and, for many Australians, whether entering the property market is possible at all.

Looking only at these figures, it can be easy to conclude that housing has become less affordable simply because homes have become more expensive.

House prices, however, are only one part of the affordability equation. Affordability is shaped by the relationship between what households earn, what homes cost and how much lenders are prepared to lend. Understanding how those three factors interact provides a much clearer picture of today's housing market than looking at the cost of living alone.

Did incomes keep pace?

If house prices are only one part of the equation, the next question is whether Australians' incomes kept pace.

According to the Australian Bureau of Statistics (ABS), average weekly ordinary time earnings for full‑time adults increased from about 1,259 dollars per week in August 2010 to 2,051 dollars per week in November 2025, an increase of around 63% over the period.

Over roughly the same timeframe, the mean Australian dwelling increased from around $450,000 to approximately $1.11 million, an increase of almost 147%.

These figures help explain why buying a home became progressively more difficult over the period. House prices increased far faster than average earnings, meaning buyers generally needed larger deposits and larger mortgages to purchase comparable homes.

But house prices are only one side of the affordability equation.

Buying a home isn't determined solely by what you earn or what a property costs. It also depends on how much a lender is willing to lend you.

That's why many Australians found themselves in a frustrating position. Their incomes had increased, yet they could borrow less than they could a few years earlier because higher interest rates and stricter lending assessments reduced their borrowing capacity.

The missing piece: borrowing capacity

Borrowing capacity is the link between what a household earns and what it can afford to buy.

When someone applies for a home loan, a lender isn't deciding whether the property is worth buying. It is deciding how much money that household can safely borrow.

The answer depends on several factors, including income, existing debts, living expenses, financial commitments and the interest rate used to assess the application. Together, these determine borrowing capacity, which is the maximum amount a lender is prepared to lend under its credit policy.

Even if two households earn exactly the same income, they may not be able to borrow the same amount if interest rates have changed. This is because lenders assess a borrower's ability to service a loan, not simply the size of their income.

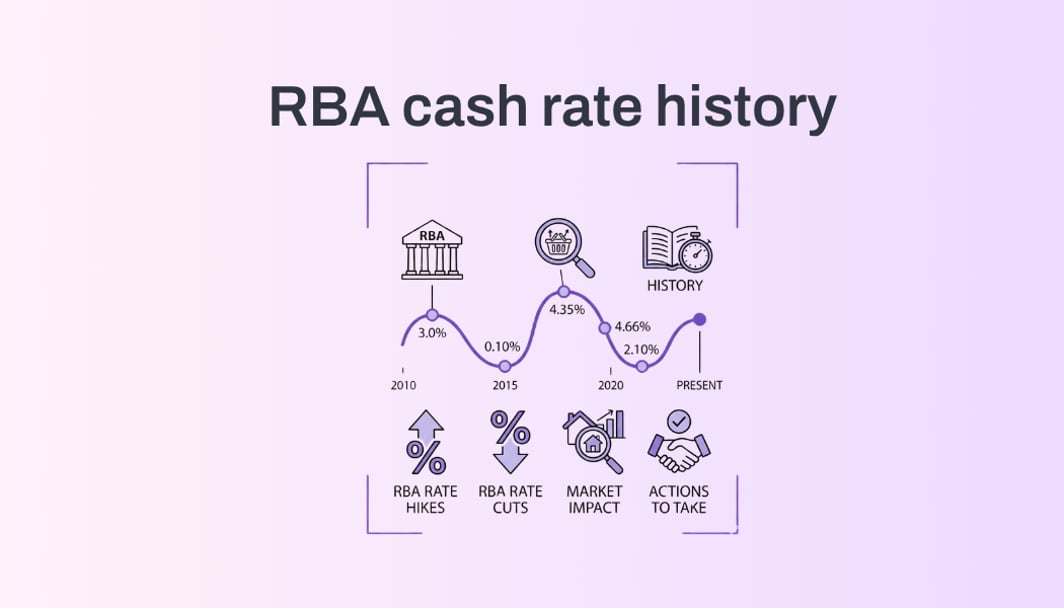

When the Reserve Bank reduced the cash rate to 0.10% during the pandemic, mortgage rates fell to historic lows. Lower interest rates reduced the repayments lenders used when assessing new loan applications, allowing many households to qualify for larger loans without any meaningful change in their incomes.

As borrowing capacity increased, more buyers were able to compete for the same pool of homes. Combined with record-low interest rates, strong demand and limited housing supply, this contributed to higher property prices.

When interest rates began rising in 2022, the process worked in reverse. Higher mortgage rates increased the repayments lenders assumed borrowers would need to service, reducing the amount many households could borrow even though incomes continued to grow. The table below illustrates how borrowing capacity changed as interest rates moved through the recent rate cycle.

*Illustrative, modelled borrowing capacity for a typical dual‑income household under standard lender servicing assumptions. Actual borrowing capacity depends on household income, living expenses, existing debts, deposit size and individual lender policies. Figures are indicative only and are included to illustrate how changes in interest rates (from around 2–2.5% in 2021 to roughly 5.5–6.0% by 2023–2026) can affect borrowing capacity over time.

Higher earnings were not enough to offset the effect of higher interest rates. Although households were earning more than before, lenders were also assuming larger loan repayments when assessing new applications. The result was that borrowing capacity declined despite continued wage growth.

Borrowing capacity therefore explains why many Australians could no longer finance homes that would previously have been within reach.

Why didn't house prices fall when borrowing capacity did?

If borrowing capacity fell so sharply after 2022, it would be reasonable to expect house prices to have fallen by a similar amount.

For a period, they did.

As interest rates rose through 2022, Australia's housing market slowed. National dwelling values fell around 7.5% between the April 2022 peak and the January 2023 trough before recovering. Higher borrowing costs reduced the amount many households could finance, fewer buyers were able to compete at previous price levels, and demand softened across much of the country. The market, however, stabilised before recovering, with national dwelling values eventually moving beyond their previous peak by November 2023.

But borrowing capacity is only one part of the story.

House prices are determined by both demand and supply. Borrowing capacity influences demand because it affects how much buyers can spend. Supply determines how many homes are available to purchase. Prices are ultimately shaped by the interaction of both.

That is broadly what occurred in Australia.

Following the reopening of international borders, population growth accelerated as migration returned to record levels. Rental vacancy rates remained exceptionally low in many parts of the country, encouraging more households to continue pursuing home ownership despite higher interest rates.

Meanwhile, the supply of new housing struggled to keep pace with demand. Construction costs increased significantly, labour shortages delayed projects, and several residential builders collapsed during the period. New housing completions remained below the level required to meet population growth, particularly in major cities.

The housing market was being pulled in opposite directions. Higher interest rates reduced borrowing capacity and placed downward pressure on prices, while strong population growth and constrained housing supply continued to support demand.

Over the past fifteen years, these forces rarely moved in the same direction. Interest rates influenced borrowing capacity. Population growth supported demand. Housing supply remained constrained. Property prices responded to all of them simultaneously.

Looking at any one of these factors in isolation explains only part of the market. Taken together, they provide a much clearer picture of why home ownership feels very different today than it did fifteen years ago.

What this means for Australians trying to buy a home

The figures in this article span more than fifteen years of Australia's housing market. During that time, incomes increased, interest rates moved from historic lows to their highest level in more than a decade, borrowing capacity expanded and contracted, and the average cost of buying a home increased by almost 150%.

No two housing cycles are identical, but the past fifteen years highlight several important lessons that remain relevant today.

1. Not all inflation affects your financial future equally

Consumer inflation and housing inflation are often discussed together, but they affect household finances in very different ways.

Rising grocery prices, electricity bills and insurance premiums reduce disposable income and place pressure on day-to-day household budgets. Housing inflation has a much longer-lasting impact. Higher property prices generally mean saving a larger deposit, taking on a bigger mortgage and paying interest on that larger loan for decades.

While managing everyday expenses is important, decisions about when you buy, how much you borrow and whether your home loan remains competitive can have a much greater impact on your long-term financial position.

2. Borrowing capacity is the missing piece

Housing affordability isn't determined by income and house prices alone. It also depends on how much a lender is willing to lend you.

Over the past fifteen years, borrowing capacity has changed significantly as interest rates and lending rules have evolved. This explains why many Australians have earned more than previous generations but still found it harder to buy a home.

Rather than relying on general market trends, it's worth understanding your own borrowing capacity. Your income, expenses, existing debts and today's lending environment all influence how much you can realistically borrow.

3. The biggest financial decisions deserve regular attention

Most Australians regularly compare supermarket prices, energy providers and insurance premiums, but many leave the same home loan untouched for years.

Yet a mortgage is often the largest financial commitment you'll ever make. Even a small reduction in your interest rate or choosing the right loan structure can save thousands of dollars over time, often far more than cutting back on everyday spending.

The biggest financial gains don't always come from spending less. They often come from making better decisions about the largest financial commitments you'll ever have.

Housing affordability isn't determined by a single number

House prices, household income, borrowing capacity, interest rates and housing supply all influence housing affordability. Looking at any one of these in isolation tells only part of the story.

While you can't control property prices, interest rates or government policy, you can understand your own position. Whether you're buying your first home, upgrading or reviewing an existing mortgage, the best decisions are based on your own borrowing capacity, financial circumstances and the lending options available today, not on headlines or assumptions.

The most valuable thing you can do isn't predict the market, it's run your own numbers. Understanding what you can borrow, what your repayments look like and whether your current home loan is still competitive puts you in a much stronger position to make confident financial decisions.

Check your borrowing capacity. It's free, and only takes a minute.

Or

Run a health check on your existing mortgage.