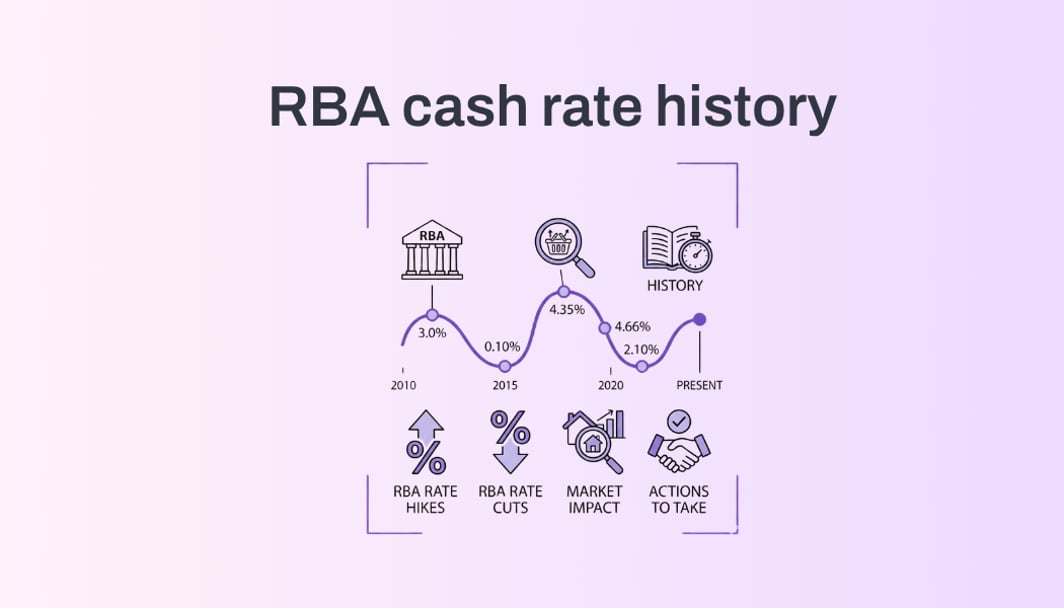

The February rate hike wasn't the peak. It was the pivot. With financial markets now pricing in an 85% probability of a 'May Spike' to 4.10%, the cost of doing nothing is about to get significantly more expensive.

According to the latest ASX 30-Day Interbank Cash Rate Futures data (as of February 19, 2026), financial markets have now priced in a 78% to 85% probability of another 0.25% hike in May.

For Australian homeowners, the "wait and see" approach is no longer a viable strategy. With the Commonwealth Bank (CBA) and NAB both forecasting a cash rate of 4.10% by mid-year, the time to stress-test your household budget is today, not when the next bank letter arrives in your mailbox.

Why May is the New Milestone?

The Reserve Bank’s recently released minutes from the February meeting confirm a "hawkish" shift. The board is increasingly concerned that inflation, particularly in the services sector (currently sitting at 4.1%), is proving far stickier than anticipated.

Three key data points are driving the May hike momentum:

- Sticky Inflation: The trimmed mean CPI, the RBA’s preferred measure of underlying inflation, has climbed back to 3.3%, moving away from the 2-3% target band.

- Labour Market Heat: January jobs data showed an unemployment rate holding steady at 4.1% with 50,000 full-time roles created, giving the RBA the "green light" to tighten further without fear of a collapse in employment.

- The Consumption Paradox: Research from the e61 Institute shows that despite past hikes, private demand remains robust because households are draining their offset accounts rather than cutting spending.

The "Assessment Gap"

Lenders typically assess your home loan application using a "floor" or "buffer" rate, usually 3% above the current product rate. As the cash rate climbs toward 4.10%, your serviceability buffer shrinks.

If you are considering a refinance or a new purchase, a May hike doesn't just increase your repayment; it slashes your borrowing power. Every 0.25% increase in the cash rate typically reduces a standard household's maximum loan capacity by approximately 2% to 3%.

How to Prepare This Month?

Don't let the "May Spike" catch you off guard. Follow these three high-intent steps:

- Run a 7.10% Stress Test: Calculate what your monthly repayments would look like if your current variable rate increased by another 0.50% (accounting for the May hike plus potential lender margin expansion). If this number exceeds 30% of your gross income, your budget is in the "danger zone."

- Request a "Loyalty Audit": Call your current lender. Competitive owner-occupier rates are still hovering around 5.50%, yet many "loyal" customers are currently sitting on 6.20% or higher. A 0.70% reduction now would completely offset the impact of the next two RBA hikes.

- Lock Your Savings, Not Your Rate: While fixed rates are rising( We are tracking here.) , your best defence is often a high-performing Offset Account. Every dollar parked there effectively earns you a "tax-free return" equal to your mortgage rate.

The Bheja.ai Solution

Navigating the May hike probability requires more than just a standard calculator. The Bheja.ai Rate Forecaster uses real-time ASX futures data to show you exactly how your specific loan will behave if the market's 85% hike prediction comes true. We can help you identify the "break-even" point where switching to a Basic Variable loan saves you more than staying with your current offset-heavy structure.

FAQ

Current market indicators from the ASX and major bank economists (CBA, NAB) suggest an 85% probability of a 25-basis point hike in May 2026, which would take the official cash rate to 4.10%.