Your home or investment property is likely your biggest asset. It's more than just a building—it's key to your financial security. In Australia, that security is under threat as bushfires and floods become more frequent and severe. Protecting your investment is a must for any responsible owner. Building and contents insurance can help, but the process can be tricky, costly, and filled with confusing terms.

Getting insurance isn't just about meeting your mortgage requirements. It's about knowing exactly what you're covered for, dealing with a changing climate, and making sure you're protected if disaster hits. Whether you own your home or rent it out, having the right insurance matters.

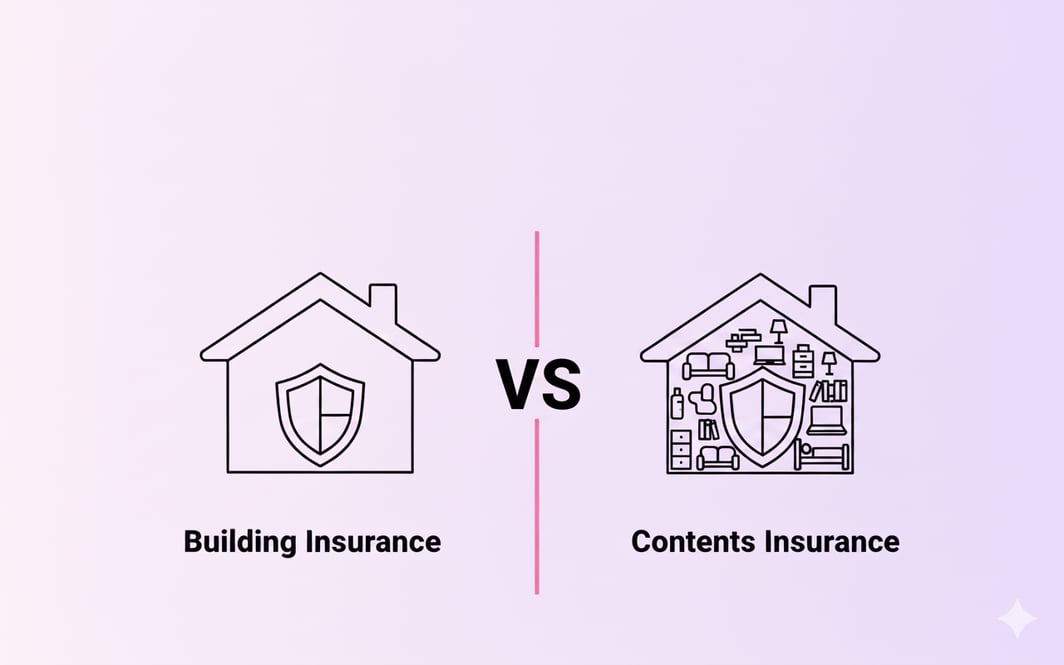

The two pillars of protection: building vs. contents

First, let's clear up the basics. People often refer to "home insurance" as a single product, but it's typically a combination of two distinct types of coverage.

Building insurance: the skeleton of your asset

Building insurance covers the physical structure of your property. Think of everything that’s fixed and not easily removed: the walls, roof, floors, windows, and doors. It also extends to permanent fixtures, such as kitchen cabinets, bathtubs, toilets, and built-in wardrobes. Outside the main house, it typically covers other permanent structures on your property, such as garages, sheds, fences, and in-ground swimming pools.

The whole point of building insurance is to cover the cost of repairing or, in a worst-case scenario, completely rebuilding your home if it's damaged or destroyed by an insured event. These events, known as 'perils', commonly include fire, storm, lightning, impact (like a car hitting your house), and malicious damage.

A common problem for homeowners is underinsurance. Many people use online calculators from insurers, but these can underestimate the real cost to rebuild, especially in areas at higher risk from natural disasters. Since 2019, building a new house in Australia has become 29% more expensive. To avoid being caught short, it's a good idea to get an independent valuation from a builder or quantity surveyor every few years. This helps make sure your insurance covers the true replacement cost.

Contents insurance: protecting what makes a house a home

Contents insurance covers your belongings inside the home. This includes everything from your furniture, appliances, and electronics to your clothes, books, and kitchenware. Essentially, if you could theoretically tip your house upside down, everything that would fall out is considered 'contents'.

This type of insurance is not just for homeowners; it is also suitable for renters. If you're a tenant, your landlord's building insurance typically does not cover your personal possessions. Renters need their own contents policy. For landlords, a contents policy can cover items they own within the rental property for the tenant's use, like carpets, curtains, and white goods.

When choosing a policy, you’ll often face a choice between 'replacement cost' and 'actual cash value' (also known as 'indemnity value'). Replacement cost coverage is generally preferable, as it pays for the full cost of replacing a damaged item with a new one. Actual cash value only pays what the item was worth at the time of the loss, taking into account depreciation. That might not be enough to buy a new fridge or television.

The new Australian reality: climate change and the cost of cover

You don't need to be a climate expert to notice Australia's weather is getting more extreme. This is already affecting insurance, with higher premiums and tougher access to coverage in many areas. Insurers are changing their policies and prices, especially for homes in flood and bushfire zones. In some high-risk places, premiums are soaring, and some insurers are pulling out, leaving some suburbs almost uninsurable.

States such as Queensland and New South Wales, which have experienced numerous recent floods and fires, are witnessing the most significant changes. Insurers are now using detailed climate risk data to set prices, so your premium depends more on the specific risks associated with your property. This can directly affect property investment returns, as higher insurance costs can reduce profit margins and overall return on investment.

In response, there is a stronger focus on resilience. The industry supports better construction standards and planning, which could help keep premiums stable over time. Government programs, such as the Disaster Ready Fund, which provides up to $200 million annually for risk reduction projects, are also helping. Some insurers now offer discounts to homeowners who take steps like adding firebreaks, flood barriers, or cyclone-rated roofing.

A landlord's guide to watertight protection

For property investors, insurance protects both the building and your income from it, as well as managing various risks associated with the property. Standard home and contents insurance is not enough. You need a specific landlord insurance policy.

Why landlord insurance is a non-negotiable

Landlord insurance is designed to cover the unique risks that come with renting out a property. A recent survey by QBE revealed that 56% of Australian landlords have this specialised cover, and for good reason. It typically includes:

- Building and Contents Cover: Similar to a standard policy, but tailored for a rental.

- Loss of Rent: If your property becomes uninhabitable due to an insured event (such as a fire), this coverage compensates for the rental income you lose while repairs are being made.

- Rent Default: This is a vital add-on. It protects you if a tenant stops paying their rent.

- Tenant Damage: This is a big one. Landlord policies differentiate between accidental and malicious damage. Accidental damage refers to an unintentional mishap, whereas malicious damage is a deliberate act of vandalism. Ensuring your policy covers both is critical.

- Liability Cover: Protects you if a tenant or visitor is injured on your property and you are found legally responsible.

Navigating the fine print: common exclusions

It's just as important to know what you're not covered for. Common exclusions in landlord policies that property managers should be aware of include general wear and tear, mould (unless caused by another insured event), and damage from building defects. Critically, a landlord's policy does not cover the tenant's personal belongings. It's best practice for investors to educate their tenants on the importance of getting their own contents insurance.

For those owning a unit or apartment, don't assume the strata insurance fully covers you. Strata insurance covers the building and common property, but there are significant gaps in coverage. It won't cover your contents within the unit (like carpets or appliances), loss of rent, or tenant-related damages. You still need a landlord policy to fill these gaps.

Your rights and protections: making the system work for you

When you buy an insurance policy, you're entering into a legal contract. Thankfully, in Australia, you're not alone. A robust legal framework exists to protect policyholders.

The law of the land: the Insurance Contracts Act 1984

The cornerstone of your protection is the Insurance Contracts Act 1984. This legislation imposes several key responsibilities on insurers. One of the most important is the duty of utmost good faith, which requires them to act honestly and fairly in all their dealings with you, especially during a claim. They must also clearly inform you of your own duties, such as the new 'duty to take reasonable care' not to make a misrepresentation when applying for cover. This replaces the old, more complex duty of disclosure and is designed to be fairer to consumers, but you must still be truthful and accurate.

Recent reforms are also targeting Unfair Contract Terms (UCT). This regime scrutinises standard form contracts to weed out clauses that create a significant imbalance in the rights and obligations between you and the insurer. Broad, vaguely worded exclusion clauses are particularly vulnerable to being deemed unfair.

When things go wrong: the claims process and disputes

No one looks forward to making an insurance claim, but understanding the process makes it easier if you need to. Good documentation is essential. For landlords, this means keeping detailed entry and exit reports with photos to show the difference between normal wear and real damage. Keep receipts, invoices, photos of damage, police reports if needed, and any related emails or letters. Staying organized with these records helps your claim go smoothly and gives you confidence if any disputes come up.

What if your claim is denied? Don't just accept it. First, ask the insurer for a detailed written explanation. Often, disputes arise from simple misunderstandings. A classic Australian example is the perennial confusion over 'flood' versus 'storm water'. Following the devastating 2022 floods, the Australian Financial Complaints Authority (AFCA) received thousands of complaints, many of which stemmed from disputes over these definitions. While the law now mandates a standard definition of 'flood', its application can still be contentious.

If you can't resolve the issue with your insurer's internal dispute resolution team, you can take your case to AFCA. This is a free, independent body that can make binding decisions on insurers.

Practical tips for smarter insurance

Navigating the insurance market can feel like a chore, but a few smart strategies can save you money and ensure you have the right cover.

- Shop Around and Compare: Don't automatically renew with your current insurer. Premiums and policies change. Use comparison websites, but also get quotes directly from insurers. Bundling your building and contents insurance with the same provider can often lead to discounts.

- Increase Your Excess: The excess is the amount you pay towards a claim, which is typically a percentage of the total claim amount. Opting for a higher excess will almost always result in a lower premium. Just make sure it's an amount you can comfortably afford to pay if you need to claim.

- Review Your Sum Insured Regularly: As mentioned, underinsurance is a huge risk. But so is over-insuring. Regularly reassess the value of your building and contents to ensure you're not paying for more cover than you need.

- Invest in Resilience: Take proactive steps to enhance your property's safety. This could mean installing security systems and smoke alarms, or for those in high-risk areas, investing in fire-resistant building materials or flood mitigation measures. Ask insurers if they offer discounts for these features.

- Read the PDS: Although it's not the most thrilling read, the Product Disclosure Statement (PDS) is your contract. Pay close attention to the definitions, inclusions, and especially the exclusions. Knowing what's not covered is just as important as knowing what is. Break it down by focusing on key sections, such as coverage, limitations, and the claims process. If the jargon feels overwhelming, consider consulting a broker or a financial advisor who can clarify the complex terms. This proactive step ensures that you're fully aware of your coverage details, avoiding unexpected surprises during claims.

Australia's insurance market is undergoing rapid changes due to climate change and economic uncertainty. Protecting your property investment is now both more challenging and crucial. By understanding the basics, staying informed about new risks, and actively managing your insurance, you can better protect your most valuable asset. It's not just about having a policy, it's about peace of mind.