When is the right time to refinance your home loan?

The best time to refinance isn't determined by the calendar or the next RBA decision. It's when your current home loan is no longer working for you. There is no one-size-fits-all answer. The right time depends on your financial situation, your goals and the home loan options available today.

Rather than asking "Is now a good time to refinance?", ask yourself: "Is my current home loan still the right one for me?"

How do you know it is time to refinance?

Most homeowners don't think about refinancing until something prompts them, a rate rise letter, a conversation with a friend who just saved $300 a month, or a fixed rate term quietly expiring. By then, many have already been overpaying for months.

Here are some signs your current loan may no longer be working for you.

Your rate hasn't been reviewed in over 12 months

Lenders quietly offer better deals to attract new customers while existing borrowers stay on older, higher rates. The gap between what loyal customers pay and what new customers are offered can be 0.5% or more. On a $600,000 loan that's around $190 every month leaving your account for no reason other than not having checked.

Your fixed rate is coming to an end

When your fixed-rate period ends, most lenders automatically move you onto their standard variable rate, which is often higher than the rates available to new customers. If you're approaching the end of your fixed term, it's worth reviewing your options 60 to 90 days before it expires. Refinancing typically takes four to six weeks, so starting early gives you time to compare lenders, complete the application and settle your new loan before your higher revert rate kicks in.

Your property has increased in value

If your home's value has increased since you bought it, your loan-to-value ratio (LVR) may have improved. A lower LVR could make you eligible for more competitive home loan products and, if you're borrowing less than 80% of the property's value, you may not need to pay Lenders Mortgage Insurance (LMI) if you refinance.

Your financial situation has changed

Your financial position may look very different from when you first took out your home loan. A higher income, paying off other debts or improving your savings could strengthen your borrowing position and make you eligible for loans that weren't available before. Equally, changes such as reduced income or additional debt can affect your refinancing options, so it's worth reviewing your circumstances before applying.

Your relationship status has changed

Major life events, such as separation or divorce, are a common reason to refinance. You may need to remove a borrower from the loan, buy out an ex-partner's share of the property or restructure the mortgage to suit your new financial circumstances. Refinancing can also be relevant if you're combining finances with a partner and want to take out a joint home loan.

You want to access the equity you've built

Equity is the difference between your property's current value and the amount you still owe on your home loan. As you repay your loan, or if your property's value increases due to market conditions, you may build equity over time.

Refinancing may allow you to access some of that equity, depending on your financial circumstances and your lender's criteria. Homeowners commonly use equity to fund renovations, purchase an investment property, pay for major expenses such as education, or consolidate higher-interest debts into their home loan.

These signs are a good starting point, but they don't automatically mean you should refinance. The next step is working out whether the savings outweigh the costs, whether you'll qualify for a better loan, and whether switching aligns with your financial goals.

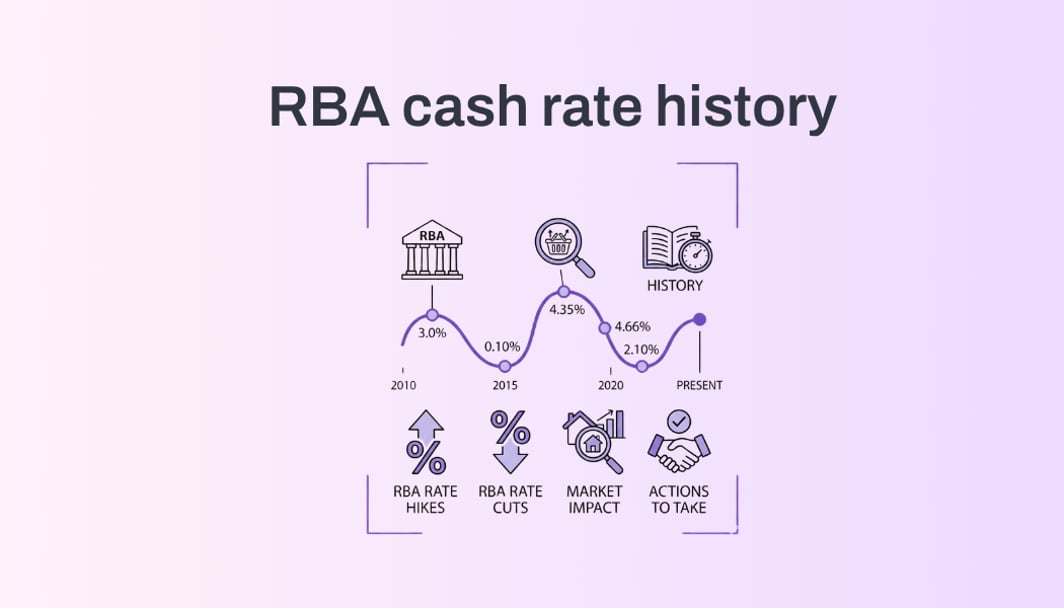

Is now a good time to refinance in 2026?

It depends on your current home loan, not just the direction of interest rates.

While the RBA has increased the cash rate in 2026, lenders continue to adjust their home loan pricing independently. Some have increased rates, others have introduced sharper pricing to attract refinancers, and not every lender responds to RBA decisions in the same way.

That means a rising cash rate doesn't automatically mean refinancing is off the table. If you've been on the same loan for several years, your fixed rate has recently expired, or your financial circumstances have improved, it's worth checking whether your current loan is still competitive.

Rather than trying to predict the RBA's next move, focus on questions you can answer today:

- Is my current interest rate still competitive?

- Would the savings outweigh the costs of refinancing?

- Am I likely to qualify for a better loan based on my current financial position?

If the answer to those questions is yes, refinancing may still be worthwhile regardless of whether rates move again later this year.

Should you wait for the next RBA decision?

Many borrowers put off refinancing because they're waiting for the next cash rate announcement. But lenders don't always move home loan rates in line with the RBA, and they don't always move by the same amount. Some lenders adjust rates before an RBA decision, others afterwards, while some choose not to pass on the full change.

That means waiting doesn't necessarily result in a better deal. If your current loan is no longer competitive, delaying a review could mean paying a higher interest rate for longer.

Rather than trying to predict the next rate move, compare your current loan against what's available today. If refinancing leaves you better off now, a future RBA decision doesn't automatically make waiting the better option.

Watch out for the loan term trap

Lower monthly repayments don't always mean you'll pay less overall.

When you refinance, some lenders may offer a new 30-year loan term by default. If you've already been paying your mortgage for several years, resetting the clock can reduce your repayments but increase the total interest you pay over the life of the loan.

Before you refinance, check both your new repayment amount and the total interest payable. If your goal is to become debt-free sooner, ask whether your remaining loan term can be matched instead of starting another 30-year term.

How Bheja helps

Knowing it's time to refinance is one thing. Working out whether it will actually leave you better off is another.

Start with a free Home Loan Health Check. Enter a few details about your current mortgage and Bheja compares it against live home loan rates from more than 100 lenders, showing whether your loan is still competitive and which products may better suit your circumstances.

If refinancing makes sense, you can securely connect your bank account using Open Banking to streamline your application. From comparison through to settlement, Bheja helps simplify the process—and continues monitoring your mortgage after settlement so you'll know when it's time to review your loan again.