Understanding mortgage repayment frequency options in Australia

- Switching from monthly to fortnightly or weekly mortgage repayments could save you tens of thousands in interest and help you pay off your home loan years sooner, provided you set up your payments correctly. Here is what every Australian homeowner should know for 2025.

- Choosing monthly, fortnightly, or weekly repayments affects how fast you pay off your loan and how much interest you save.

- Aligning repayments with your pay cycle can help with budgeting.

Why repayment frequency matters

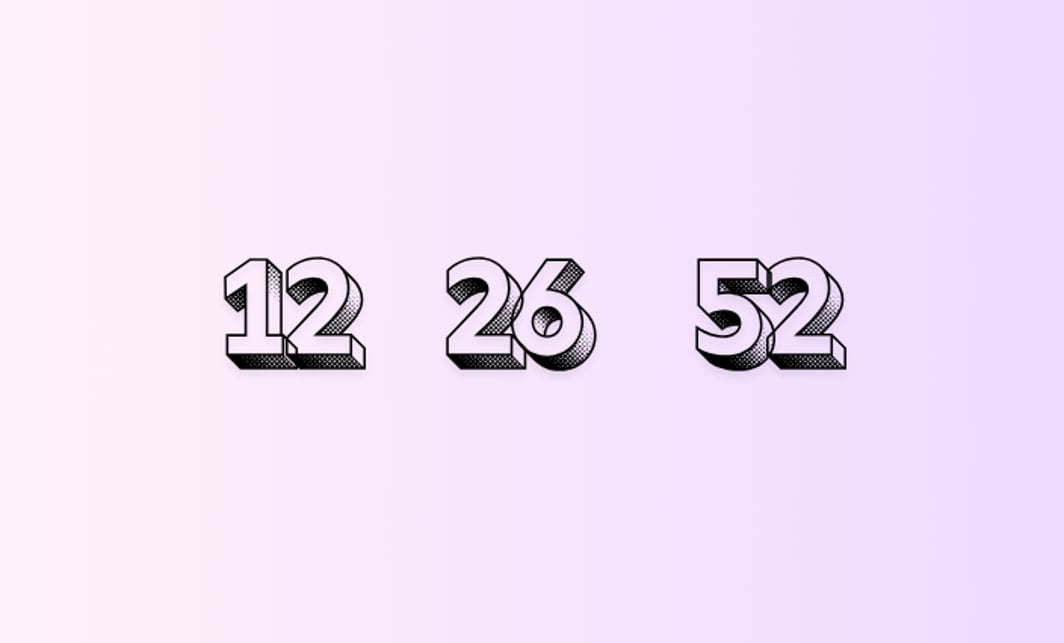

When you take out a home loan in Australia, you usually have three options for how often you repay it:

- Weekly (52 payments/year)

- Fortnightly (26 payments/year)

- Monthly (12 payments/year)

Most borrowers opt for monthly payments by default; however, this decision can ultimately result in higher costs over time.

How does repayment frequency affect your loan?

Choosing the right repayment frequency is not just about convenience; it's also about achieving financial stability. It can significantly affect the total interest you pay, the length of your loan, and your ability to manage cash flow.

- Interest Costs: More frequent repayments reduce the outstanding principal faster, leading to lower interest accrual.

- Loan Term: Accelerated principal reduction shortens the duration needed to repay the loan fully.

- Financial Management: The frequency of repayments affects your ability to budget and your comfort with your finances. It can also influence your motivation to stick to your repayment plan.

Understanding how these factors operate can help Australian mortgage holders and first-home buyers in 2025 maximise the benefits of their home loans, particularly as the financial landscape continues to evolve.

Case study: Emma’s $600K home loan

Emma took out a 30-year home loan of $600,000 at an annual interest rate of 6.25%.

Here’s what her repayments looked like across different schedules:

By simply making more frequent repayments, Emma can save over $69,000 in interest and pay off her loan 3 years early. Check out how much you could save by switching repayment frequency using our health check calculator.

How Does This Work?

Fortnightly = 13 Months in a Year?

Yes—when you split your monthly repayment in half and pay it every 2 weeks, you end up making 26 half-payments, or 13 full months of repayments in a year. That’s one extra month paid off annually without changing your budget.

This extra payment reduces your principal faster, so you pay less interest over time.

By simply making more frequent repayments, Emma can save over $69,000 in interest and pay off her loan 3 years early. Check out how much you could save by switching repayment frequency using our health check calculator.

What to watch out for when choosing repayment frequency?

Even though more frequent repayments can save interest, there are a few lender-specific factors that could reduce or offset those savings:

1. Fees for Changing Repayment Frequency

2. Interest Calculation Method: Lenders' interest calculation methods (daily vs monthly) substantially influence the benefits of frequent repayments.

If your lender calculates interest daily, you get the most benefit from weekly or fortnightly repayments. Each payment quickly reduces your loan balance, so you pay less interest overall. This can sometimes result in a saving of 2 to 4 percent over the life of your loan compared to the monthly interest.

Conversely, lenders using a monthly interest calculation offer limited additional savings from more frequent repayments, as interest is based on the opening balance each month.

Tip: Always ask your lender which method they use.

3. Other Fees and Costs

Tip: Always check the fine print before deciding to switch to avoid any unexpected costs.

How repayment frequency affects budgeting and financial behaviour

Cash flow management and flexibility with frequent repayments

Let’s say you’re paid your salary fortnightly. Matching your loan repayments with your pay cycle helps you stay on track and avoid late payments.

Example: Managing a budget with weekly repayments

Josh earns $3,600 every fortnight.

He switched from a $3,600 monthly repayment to a $1,800 fortnightly repayment.

Result?

- He found it easier to manage bills.

- Paid off his loan faster

- Felt less stressed about money

Behavioural science: Benefits of smaller, more frequent repayments

Behavioural science shows that making smaller, more frequent payments helps people stick to their repayment habits. Breaking up a big monthly payment into weekly or fortnightly amounts gives you more chances to feel like you’re making progress and staying in control.

- Regular, smaller payments also reduce the mental burden and psychological discomfort (“pain of paying”) felt with larger, less frequent payments, increasing repayment adherence by up to 12% compared to monthly schemes.

- Frequent payments foster a sense of progress and control, encouraging disciplined financial behaviour and reducing payment procrastination.

- Monthly repayments can decrease motivation due to larger, less frequent payments that may feel overwhelming or disconnected from income flows.

These behavioural advantages translate into lower default risks and better loan performance.

How repayment frequency impacts savings, investments, and emergency funds

Repayment schedules also influence borrowers’ ability to save, invest, and maintain emergency funds:

- Frequent repayments reduce total interest paid, freeing up future cash flow for savings and investments.

- Weekly and fortnightly payments align with income cycles, improving liquidity and enabling borrowers to maintain higher emergency fund balances (up to 15% higher than monthly payers).

However, more frequent payments require disciplined budgeting to avoid liquidity issues, especially for borrowers with irregular incomes. Those with stable incomes may use frequent repayments for wealth accumulation, while borrowers with variable incomes might prefer monthly schedules to preserve short-term liquidity.

Behavioural barriers and strategies for transitioning repayment frequencies

Despite the financial benefits, many Australian borrowers face behavioural hurdles when switching repayment frequencies:

To address these, lenders and policymakers implemented evidence-based strategies in 2025:

- Simplifying switching processes through automation and borrower consent.

- Using framing techniques emphasising long-term savings.

- Deploying commitment devices and financial literacy programs tailored to mortgage holders.

- Introducing digital tools and apps to improve repayment tracking and engagement.

These interventions have helped increase the adoption rates of weekly and fortnightly repayments by up to 15% among new borrowers.

How lenders and the market view repayment frequency

How frequent repayments impact the Australian housing loan market

Widespread adoption of weekly and fortnightly repayments yields positive macroeconomic effects:

- Accelerated principal reduction lowers household debt burdens and default risk, improving financial stability.

- More frequent payments smooth household cash flows, reducing missed payments and non-performing loans.

- These factors contribute to improved housing affordability and sustainable homeownership, especially for new borrowers.

Studies show switching to weekly repayments can reduce total interest by 5-7% and shorten loan terms by 3-4 years, positively impacting the housing finance ecosystem.

How lenders assess risk and set interest rates based on repayment frequency

Lenders integrate repayment frequency into risk assessment and pricing:

- Frequent repayments reduce default risk, allowing lenders to offer marginally lower interest rates and fees for weekly or fortnightly schedules.

- Pricing strategies reflect risk-adjusted expected losses, incentivising borrowers to choose repayment frequencies that enhance loan performance.

- Regulatory oversight ensures transparency and fairness in pricing related to repayment schedules.

Transparency and consumer information about repayment frequency

Australian lenders have improved transparency regarding repayment frequency options:

- Many provide clear, accessible information about benefits, drawbacks, fees, and administrative conditions.

- Regulatory bodies, such as ASIC and ACCC, monitor disclosures to ensure that consumers make informed decisions.

- Some gaps remain in communicating potential budgeting pressures and fee structures associated with frequent repayments.

Continuous efforts are underway to enhance borrower education and support informed decision-making.

Summary of key points on repayment frequency

Key findings on repayment frequencies

- Weekly or fortnightly repayments offer substantial interest savings (3-15%) and loan term reductions (2-4 years) compared to monthly repayments.

- Daily interest calculation by lenders maximises these savings.

- More frequent repayments improve cash flow management, budgeting flexibility, and borrower motivation.

- Lenders adjust risk assessment and pricing favourably for borrowers adopting frequent repayment schedules.

- Behavioural barriers exist but are being addressed through digital tools, financial education, and automated switching.

- Transparent lender communication remains critical for informed borrower choices.

Practical guidance for borrowers

- Assess your income cycle: weekly or fortnightly repayments align better with frequent income streams.

- Consider lender interest calculation methods; prefer lenders that calculate interest on a daily basis.

- Review lender fees and policies related to repayment frequency to avoid eroding savings by switching.

- Use digital budgeting tools to manage smaller, frequent payments effectively.

- Consult a mortgage broker to model savings and tailor repayment frequency to your financial goals.

- Maintain an emergency fund to manage cash flow variability.