Refinancing your home loan at the right time could save you tens of thousands of dollars over the life of your mortgage. Whether you’re in Lane Cove, Sydney, or anywhere in Australia, understanding the key triggers and market conditions can help you lock in a better rate, access equity, or simplify your repayments.

In this 2025 guide, we’ll show you exactly when refinancing makes sense, the costs you should know about, and how to check if it’s worth it using our Free Home Loan Health Check.

8 Signs It’s the Right Time to Refinance Your Home Loan

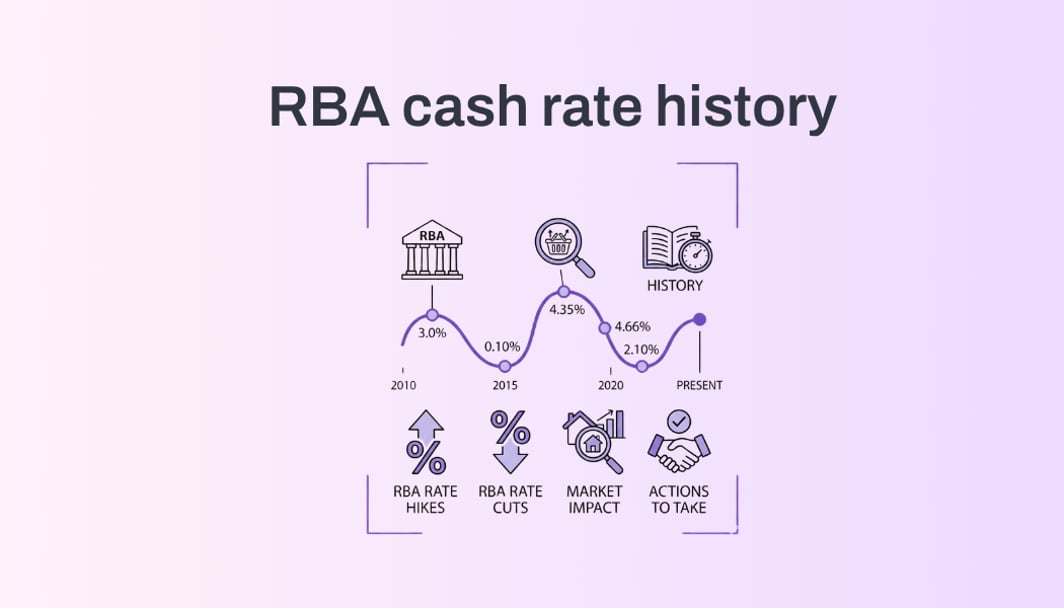

1. Interest Rates Have Dropped After RBA Cuts

If your current interest rate is higher than what lenders are offering today, refinancing could cut your repayments significantly. Even a 0.5% drop could mean $200+ per month in savings on a $600,000 loan.

2. Your Fixed Rate Is About to End

Coming off a fixed rate often means being moved to a higher revert rate. Refinancing before that happens lets you lock in a more competitive deal.

3. Your Property Value Has Increased

A higher valuation can:

- Reduce your Loan-to-Value Ratio (LVR) and avoid Lenders Mortgage Insurance (LMI)

- Qualify you for lower interest rates

- Unlock equity for renovations or investments

4. Your Financial Situation Has Improved

Better credit score? Higher income? Lower debts? You could now qualify for premium loan features and lower rates.

5. You Want to Consolidate Debt

Combining personal loans, credit cards, and your home loan into one lower-rate repayment can simplify your finances and reduce interest.

6. You Need More Flexible Loan Features

Offset accounts, redraw facilities, and better online banking tools might be available through other lenders — potentially at a lower cost.

7. You’re Paying for Extras You Don’t Use

Why pay annual package fees for features you never use? A no-frills, low-fee loan might suit you better.

8. Cashback Offers Are High

Some lenders offer $2,000–$4,000 cashback to switch. If rates are also competitive, it’s worth considering.

Example: How much could you save?

Let’s say you have a $600,000 home loan at 6.40%.

Refinancing to 5.89% could save you:

- $200+ per month

- $70,000+ over the loan term

Refinancing costs you should consider

Refinancing isn’t free. To determine if it’s worth it, factor in these common costs:

- Refinancing isn’t free. Factor in:

- Discharge fees: $350–$500

- Application fees: $0–$750 (often waived)

- Property valuation fees

- Government charges: $130–$240

- Settlement/legal fees

- Break costs (if fixed rate)

- LMI if LVR > 80%

📌 Tip: Use our Home Loan Health Check to calculate savings after fees.

Is it the right time for you?

There’s no one-size-fits-all answer. The best time depends on:

- Your current rate vs market offers

- Your future plans (selling, investing, renovating)

- The cost of switching vs potential savings

Most Australians refinance around 5 years after purchase, but market changes — like RBA cash rate cuts — can make earlier switching worthwhile.

Take the First Step: Free Home Loan Health Check

Don’t guess — run the numbers. Our quick Home Loan Health Check will tell you:

- If refinancing will save you money

- How much you could save monthly & over the loan term

- Your best refinance options in today’s market

FAQ: Refinancing in Australia 2025

A: If rates are lower than what you’re paying, your equity has grown, or your fixed term is ending, 2025 could be an ideal time to refinance.