In the world of pest control, there’s an old saying: "If you see one cockroach, there are ten more behind the fridge."

Economists often apply this same logic to interest rates. When a central bank like the Reserve Bank of Australia (RBA) raises the cash rate after a long pause, it’s rarely a one-off event. In finance, this is known as the "Cockroach Effect”. The idea that the first hike is simply the one that was brave enough to scurry out into the light, signalling that a whole "colony" of further increases is likely hiding in the data.

Historical infestations: When the cockroaches multiplied

History shows that central banks almost never stop at one. Once the cycle begins, it tends to gain momentum as the underlying issues (usually stubborn inflation) prove harder to "exterminate" than first thought.

- The 1994 "Great Bond Massacre": The U.S. Federal Reserve surprised markets with a modest 0.25% hike in February 1994. Investors thought it might be a solo move. Instead, it was the first of seven hikes in a single year, doubling the rate from 3% to 6% and sending global bond markets into a tailspin.

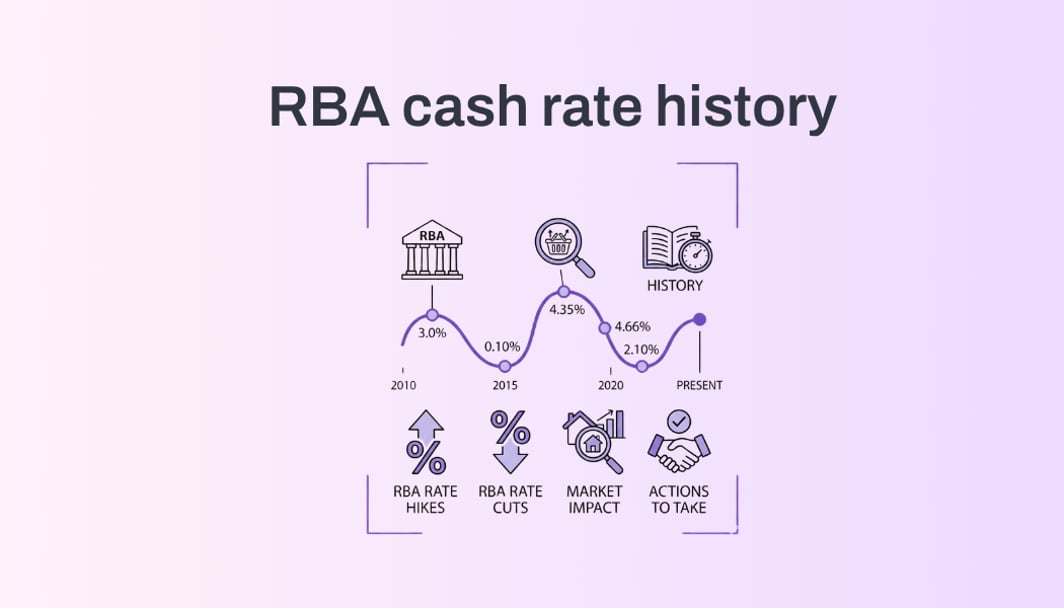

- The RBA’s 2022 Cycle: After years of record-low rates at 0.1%, the RBA "saw the first cockroach" in May 2022. That single 25-basis-point move didn't stay lonely for long; it kicked off a historic streak of 12 increases that didn't stop until the rate hit 4.35% in late 2023.

- The Volcker Era (1979): The most famous example of "pest control." Fed Chair Paul Volcker realised that small, sporadic hikes weren't working. He eventually pushed rates to 20% to finally kill off the inflation that had infested the 1970s economy.

Review of the Reserve Bank of Australia Annual Report 2025

Based on the testimony from the House of Representatives Standing Committee on Economics on February 6, here is how the "Cockroach Effect" is playing out in the 2026 scenario.

The February 2026 Hike

The RBA’s decision on February 3, 2026, to lift the cash rate to 3.85%, the first increase in over two years, has many wondering if the "cockroaches" are back. Appearing before the House of Representatives Standing Committee on Economics on February 6, RBA Governor Michele Bullock acknowledged that this rate hike may not be a one-off.

The nest behind the fridge: Excess demand

Governor Bullock revealed that the "infestation" is worse than previously thought. While inflation had fallen from its 2022 peaks, it "picked up materially" in late 2025, driven by unexpected strength in household consumption and business investment. The Governor addressed the cause, noting that: "aggregate demand... is currently in excess of the ability of the economy to supply those goods and services".

A colony of hikes in the data

Crucially, the "Cockroach Effect" was all but confirmed when the RBA discussed its future outlook. Governor Bullock admitted that their current economic forecasts now rely on a "technical assumption where the interest rate is going up".

When pressed by committee member Mr Kennedy on whether the bank would need "at least one to two rate hikes if not more" to tame inflation, the Governor confirmed that their modelling relies on a market path that assumes exactly that.

With the RBA not expecting inflation to return to its target band until 2028, marking six years of missed targets, it appears the exterminators will be working on this infestation for some time to come.

What this means for you

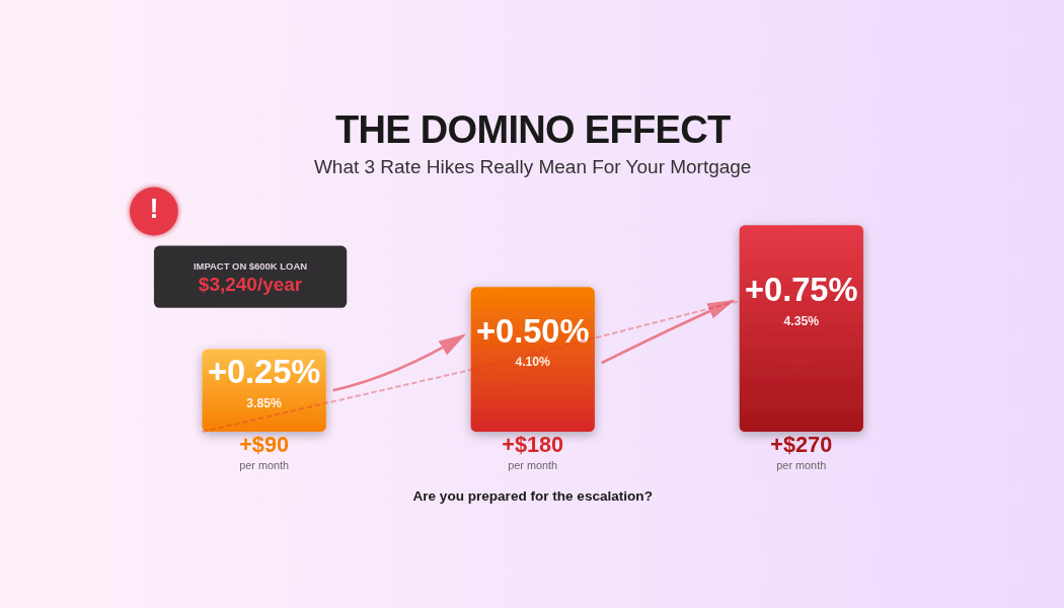

If the Cockroach Effect holds true in 2026, the current hike to 3.85% is likely just the beginning of a mini-colony. Major banks, including CBA, are already forecasting a follow-up hike as early as May, potentially taking the rate to 4.10%.

The Domino Effect on Your Finances:

- Mortgages: Expect your variable rate to jump almost immediately. If you have a $750,000 loan, this single hike adds roughly $120 to your monthly bill. Three hikes? That’s nearly $400 extra every month.

- Credit & Loans: Personal loan and credit card rates often follow the cash rate upward, making "convenience" debt much more expensive.

The Opportunity: If you’re a saver, this is finally some good news. However, the real "pro move" right now is to stress-test your budget. Don’t wait for the second or third cockroach to scurry across the floor. Check your finances now: if rates climb another 0.50% or 0.75% this year, could your lifestyle handle the "infestation"?

Staying ahead of the curve is the only way to ensure your budget doesn't get bitten.