Key Takeaways

- HEM stands for Household Expenditure Measure. It is the benchmark Australian banks use to estimate your minimum living expenses during a home loan assessment.

- If your declared expenses are lower than HEM, the bank will use HEM instead, which can reduce your borrowing capacity.

- HEM is controversial. The Banking Royal Commission found that some lenders were using it as a shortcut, making it easier to approve loans that borrowers couldn't really afford.

- Understanding HEM before you apply can help you present your finances more accurately and potentially borrow more.

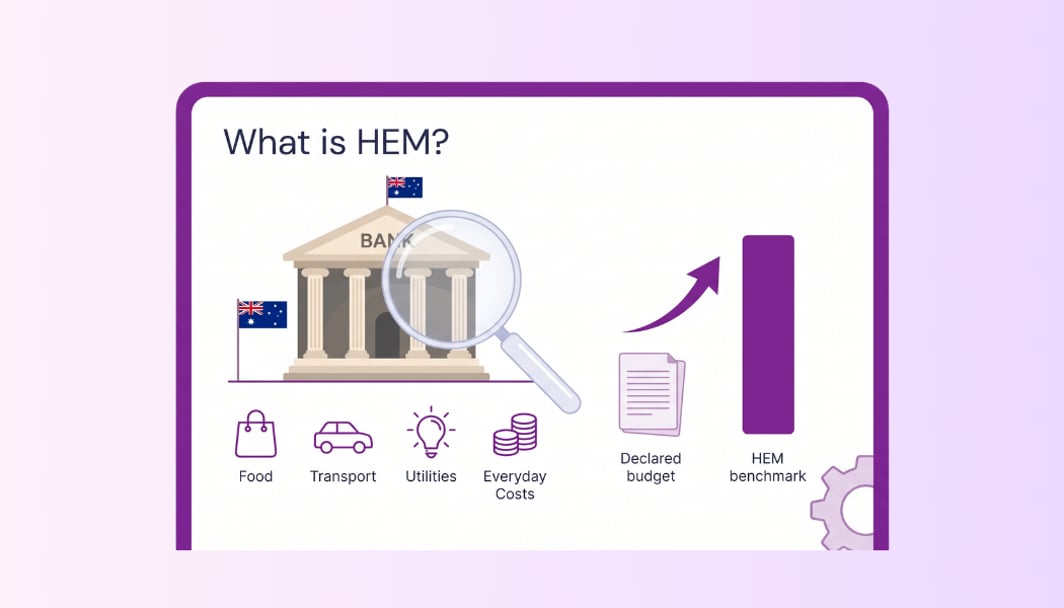

What is HEM?

HEM (the Household Expenditure Measure) is a spending benchmark developed by the Melbourne Institute of Applied Economics and Social Research. Australian banks use it to estimate the minimum a household is likely to spend on living expenses each month.

In plain English: when you apply for a home loan, your lender needs to know you can afford the repayments after paying for food, transport, utilities, and other everyday costs. Rather than taking your word for it, most banks check your declared expenses against HEM. If your numbers look too low, they'll use HEM instead.

It is not a figure the bank publishes or shows you. It runs silently in the background of almost every home loan assessment in Australia.

Why do banks use HEM?

Under Australia's responsible lending laws (National Consumer Credit Protection Act 2009), lenders must verify that a loan is "not unsuitable" for the borrower. That means they cannot just look at your income. They must also assess your expenses.

Checking every borrower's actual spending would require months of bank statement analysis. HEM gives lenders a standardised minimum to work with quickly.

Around 70–80% of Australian lenders use HEM as a benchmark. Some use it exclusively; others use it as a floor alongside your declared expenses, taking whichever is higher.

How is HEM calculated?

HEM is built from the Australian Bureau of Statistics Household Expenditure Survey, which is conducted every six years. The Melbourne Institute updates HEM quarterly to adjust for inflation.

The benchmark splits household expenses into three buckets:

HEM is deliberately modest. It reflects what a frugal household spends, not what the average Australian actually spends. This is a key point: HEM is a minimum, not an average.

Your HEM figure varies based on:

- Household size (single, couple, family)

- Number of dependants

- Whether you live in a capital city or a regional area

- Your gross income (higher earners have slightly higher HEM benchmarks)

The "Wagyu and Shiraz" Case: Why HEM became controversial?

The most famous legal battle over HEM in Australia was ASIC v Westpac, heard in the Federal Court in 2019.

ASIC argued that Westpac had approved home loans for borrowers who could not genuinely afford repayments, partly because the bank relied too heavily on HEM rather than verifying actual expenses. The judge sided with Westpac, famously stating that a borrower should not be assessed on the assumption they would continue eating "wagyu beef and drinking Shiraz" after taking out a mortgage.

ASIC appealed and lost again. The case effectively confirmed that lenders can use HEM as a reasonable baseline, but the Banking Royal Commission had already shone a harsh light on the practice.

The Royal Commission found that lenders were routinely using HEM as a rubber-stamp shortcut, making loans appear affordable when they were not. Since then, ASIC and APRA have tightened expectations around expense verification, and most lenders now do both: they check bank statements and cross-check with HEM.

How does HEM affect your borrowing capacity?

Here is where it gets practical.

If you declare your monthly living expenses as $2,800 but HEM for your household profile is $3,400, your lender will assess you as if you spend $3,400. That extra $600/month reduces the surplus income available for mortgage repayments, which directly cuts your maximum borrowing limit.

Worked example

Household: Couple, two children, living in Sydney.

Combined gross income: $180,000/year

Declared monthly expenses: $2,900

HEM benchmark for this profile: $3,700 (approximate)

Difference: ~$130,000 in borrowing capacity.

This is not a hypothetical edge case. Most Australians underestimate their actual spending when filling out a loan application. HEM often ends up above what they declare, not below. The bank then uses the higher number, and your borrowing power shrinks accordingly.

What counts in your declared expenses?

When you apply for a home loan, your lender will ask you to estimate your monthly spending across categories, including:

- Groceries and household goods

- Utilities (electricity, gas, water, internet)

- Transport (petrol, registration, public transport)

- Education (school fees, uniforms, extracurriculars)

- Insurance (health, car, life)

- Personal spending (clothing, haircuts, subscriptions)

- Childcare and dependent costs

- Entertainment and dining out

- Gym memberships and recreation

The key rule: be accurate, not strategic. Declaring unrealistically low expenses does not help you. It triggers HEM anyway, and it may also be flagged as a compliance issue when the bank reviews your bank statements.

How to work with HEM, not against it

1. Know your HEM before you apply

While banks do not publish their specific HEM tables, you can get a reasonable estimate from a mortgage broker before lodging an application. Bheja.ai's borrowing capacity calculator uses expense inputs to show you how different spending levels affect your maximum loan amount, so you can see the impact before it matters.

2. Declare your expenses accurately

If your actual expenses are genuinely higher than HEM (which is likely in most Sydney or Melbourne households), declare them accurately. A higher declared expense figure is only a problem if it makes you unserviceable. Knowing that before you apply means you can address it rather than face a surprise rejection.

3. Reduce discretionary spending before applying

Lenders look back 3–6 months on your bank statements. If you have a pattern of high discretionary spending, such as frequent dining out, subscriptions or luxury purchases. Trimming these for a few months before applying can lower your actual declared expenses, bringing them closer to or below HEM.

4. Choose your lender carefully

Different lenders shade HEM differently. Some use a strict interpretation; others apply their own internal benchmarks that are more generous for certain borrower profiles (e.g., self-employed borrowers with variable income). A mortgage broker who knows how each lender applies HEM can match you with the right one for your situation.

5. If you are self-employed

HEM can be particularly tricky for self-employed borrowers. Your declared business and personal expenses sometimes overlap, and lenders may assess your income conservatively (a practice known as income shading). Make sure your personal and business expenses are clearly separated, and that your accountant's records reflect your actual living costs, not just what was tax-optimised.

HEM vs Your Actual Expenses: Which does the bank use?

Most lenders follow this simple rule:

They use whichever is higher: your declared expenses or HEM.

If your declared expenses are below HEM, HEM wins. If your declared expenses are above HEM, your declared amount wins (assuming it is supported by bank statements).

A small number of lenders have moved away from HEM entirely and use their own internal expense benchmarks based on more granular data. A few non-bank lenders are even more flexible. Your broker can tell you which approach a specific lender uses before you apply.

Frequently Asked Questions

How Bheja.ai Can Help

Working out how HEM affects your specific borrowing capacity across more than 100 lenders is exactly what Bheja.ai is built for.

Our borrowing power calculator lets you enter your household expenses and see your borrowing capacity change in real time. And if you want to understand which lenders apply HEM more generously for your profile, our AI assistant can walk you through the options before you make a single application.

Calculate your borrowing power →

Ask Bheja about your expenses →

This article provides general information only. It does not constitute financial advice. Bheja Group Pty Ltd (ABN 31683827938) is a Corporate Credit Representative (CR 570637) of Purple Circle Financial Services Pty Ltd (ACL 486112). Always seek independent financial advice before making borrowing decisions.