What is negative gearing?

Gearing simply means borrowing money to buy an investment asset, like a property. When a property is negatively geared, it means the money you earn from that property (the rent) doesn't cover the total cost of owning it. The property runs at a loss on a cash flow basis, and under Australian tax law, that loss can normally be offset against your other income, reducing the amount of tax you pay.

The costs that create the loss typically include:

- Loan interest payments (the largest component)

- Property management fees

- Council rates and water charges

- Repairs and maintenance

- Landlord insurance

- Depreciation on the building and fittings

If your rental property earns $28,000 per year in rent but costs you $42,000 per year to hold (mostly in interest), you have a $14,000 net rental loss. Under the old rules, that $14,000 reduces your taxable income, saving you tax at your marginal rate. On a $150,000 salary, that is a tax saving of approximately $6,370 per year at the 47% combined marginal rate.

How negative gearing affects your borrowing capacity

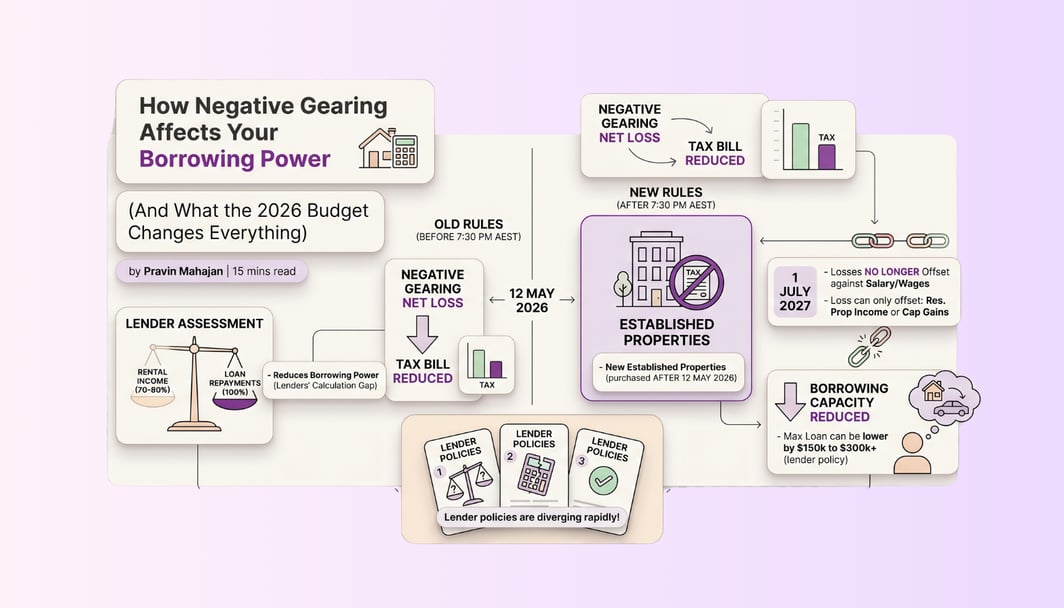

When you apply for a loan, lenders run a serviceability assessment: your total income minus your committed expenses. A negatively geared property impacts both sides of this equation. On the income side, lenders apply "rental shading," counting only 70% to 80% of your gross rent to factor in vacancies and property fees.

On the expense side, your investment loan repayments are counted in full and stress-tested at a higher interest rate. The gap between your shaded rent and stress-tested repayments creates a cash-flow shortage, reducing the surplus income available for your next loan.

However, some lenders help close this gap by adding your negative gearing tax refund back into your assessed income. For example, if a property runs at a $14,000 annual loss but your tax refund is $6,370, these lenders calculate your real cash-flow cost as $7,630 instead of $14,000. Choosing a lender that applies this tax add-back can boost your maximum loan amount by $100,000 or more.

The 2026 budget: What changed on 12 May and what It means for borrowing

The 2026 Federal Budget, announced at 7:30 pm AEST on 12 May 2026, introduced the most significant change to negative gearing in nearly a century.

The key rule change

From 1 July 2027, rental losses on established residential investment properties purchased after 7:30 pm AEST on 12 May 2026 can no longer be offset against salary, wages, or other non-property income. Instead, those losses can only be applied against:

- Other residential rental income (from any properties in your portfolio)

- Capital gains from the sale of a residential rental property

Any excess losses that cannot be used in the current year are carried forward to future years. They do not disappear, but the immediate tax benefit on your annual return is gone.

What is still exempt

New builds remain fully exempt from the new rules. If you purchase a newly constructed property that adds to the housing supply, you can still offset rental losses against your salary income as before. This is a deliberate policy lever designed to encourage new construction rather than competition for existing stock.

What is grandfathered

Properties purchased or under contract before 7:30 pm AEST on 12 May 2026 are not affected. The old rules continue to apply to those properties until they are sold.

The grace period: 12 May 2026 to 30 June 2027

Properties purchased between Budget night and 30 June 2027 are subject to a short grace period. They can be negatively geared under the current rules during that window. From 1 July 2027, the new quarantine rules apply.

The CGT change that runs alongside

The Budget also replaced the existing 50% CGT discount with cost base indexation plus a 30% minimum tax on net capital gains, effective from 1 July 2027. For properties purchased after Budget night, the exit calculation changes significantly. Speak to your accountant about this before making any purchase decision. The interaction between the new negative gearing rules and the new CGT rules is complex.

How the 2026 budget changes impact your borrowing capacity?

The 2026 Budget changes may affect borrowing capacity for some investors, especially as lenders remove or reduce the tax add-back used in serviceability assessments for newly purchased established properties.

Early broker estimates suggest the impact could be significant, but the exact reduction will depend on the lender, the borrower’s income and debts, and how quickly each bank updates its policy. For example, one major broker firm estimated that removing the tax benefit could reduce the maximum investment loan for a borrower on a $150,000 salary from about $750,000 to $600,000.

Another analysis found borrowing capacity reductions of up to 30% for investors who rely heavily on the tax benefit in serviceability assessments.

Of course, serviceability criteria differ between lenders, so a good broker may know which lenders are likely to look more favourably on your situation.

Your situation: which scenario applies to you?

1. You already own investment properties bought before Budget night

If all your current investment properties were purchased or under contract before 7:30 pm on 12 May 2026, nothing changes for those properties. You continue to offset rental losses against your salary income as before, until you sell.

Your borrowing capacity for a newly established property, however, will be assessed under the new rules if you purchase after Budget night. Consider whether a new build is a better fit for your next purchase, given the continuing tax treatment.

2. You're looking to buy an established property now

You are in the most directly affected group. Rental losses on any established property you purchase after Budget night will be quarantined from 1 July 2027. The immediate tax benefit that has historically improved your serviceability will no longer be available for lender assessments going forward.

The key question to raise with your broker: which lenders have updated their models to reflect the new rules, and which are still using the old calculation? The answer could be worth six figures in borrowing capacity.

3. You're considering a new build

New builds are the clear beneficiary of the Budget change. Not only do they retain full negative gearing treatment against all income, but investor demand for established properties is likely to fall, while demand for new builds increases.

Be aware that new-build prices may rise to absorb this shift in demand, and that construction costs remain elevated in 2026. Run your numbers carefully before assuming a new build is automatically cheaper to hold.

How investors can tweak their strategy in the new environment

1. Find out which lenders are still applying the old tax add-back

Lender policies are changing swiftly. A broker with current access to lender credit teams can tell you which lenders are still applying the tax add-back for established properties, and which have already moved to a post-budget model. This information isn't publicly available and changes week to week.

2. Consider interest-only structuring on investment loans

Using interest-only repayments on your investment loan reduces the assessed monthly repayment in the lender's serviceability calculation compared with principal-and-interest repayments. This can preserve borrowing capacity for your next purchase.

That said, interest-only periods are typically limited to 5 years on investment loans, and the switch to principal-and-interest repayments will increase your repayments at the end of that period.

3. Separate your owner-occupier and investment loan applications carefully

Many lenders assess your entire debt portfolio simultaneously when you apply for any new loan. The order in which you take on debt and the structure of each loan can meaningfully affect your maximum borrowing capacity.

A broker who understands sequencing, which loan to get first, at which lender, in which structure, can unlock significantly more borrowing capacity than applying to your existing bank directly.

4. Maximise your rental income evidence

Because rental shading reduces your counted income, the quality of your rental evidence matters. A formal property manager's rental appraisal that documents current market rent (rather than just your old lease) can help with lenders who use the higher of actual versus appraised rent. If your property has been tenanted below market rates, getting an updated appraisal before applying is worth the effort.

5. Model the total return, not just the tax benefit

With the immediate tax offset gone for newly purchased established properties, the case for negative gearing now rests almost entirely on capital growth. Before purchasing, model a scenario with modest capital growth (3-4% per year) and ask whether the cash flow cost is sustainable over 10 years without the annual tax refund as a buffer. If the answer is no, the investment may not be suitable in the new environment.

Looking for some help?

Run the numbers using our in-depth tools to get the answers you seek.

Calculate your investor borrowing power

Talk to Bheja about your investment strategy

Frequently Asked Questions

Negative gearing is when the costs of owning an investment property — including loan interest, management fees, rates, repairs and depreciation — exceed the rental income it generates. The resulting net loss can normally be offset against your salary and other income, reducing your tax bill. Under the 2026 Budget proposals, this offset will be restricted for established properties purchased after Budget night from 1 July 2027, though the legislation has not yet passed Parliament.

This article provides general information only. It does not constitute financial advice or tax advice. Tax laws change and the 2026 Budget measures described above are subject to the passage of enabling legislation. Bheja Group Pty Ltd (ABN 31683827938) is a Corporate Credit Representative (CR 570637) of Purple Circle Financial Services Pty Ltd (ACL 486112). Always seek independent financial and tax advice before making investment decisions.