Key points:

- Three RBA rate hikes in 2026 have already cut borrowing capacity for the average household.

- Budget 2026 restricts negative gearing for new eligible property purchases from 1 July 2027, with grandfathering for existing owners. Some lenders may also update their borrowing calculations, which could affect borrowing power for new applications.

- Selling an investment property after 1 July 2027 may affect your tax outcome, depending on how the new rules apply to your circumstances.

- First home buyers may actually benefit, but rate hikes are hurting them, too.

- A mortgage broker can help you figure out where you stand and what to do next.

Why some investors are seeing their borrowing power shrink?

If you own an investment property, or were planning to buy one, here's something you need to know right now: the rules just changed. Significantly.

In the space of a few weeks in May 2026, two things happened that hit investors from two different directions at once. The RBA raised interest rates for the third time this year. And the federal Budget rewrote how banks may calculate what you can borrow as a property investor.

The result? Brokers are calling it one of the biggest overnight shifts to investor borrowing power they've ever seen.

What actually changed, and why it matters to you

The rate hikes: your borrowing power is already down $36,000

The Reserve Bank has raised the cash rate three times in 2026, in February, March, and May, taking it from 3.60% back up to 4.35%. That's the same level as the peak of the previous rate cycle in 2023-24.

Each time the RBA moves, the banks move with it. And when your mortgage rate goes up, banks recalculate how much you can safely borrow.

According to Cotality's housing trends data, each 0.25% rate rise cuts borrowing capacity for a median-income household by around $18,000. Across three hikes, that's roughly $36,000 gone from the average Australian household's borrowing capacity, and that's before we get to the budget changes.

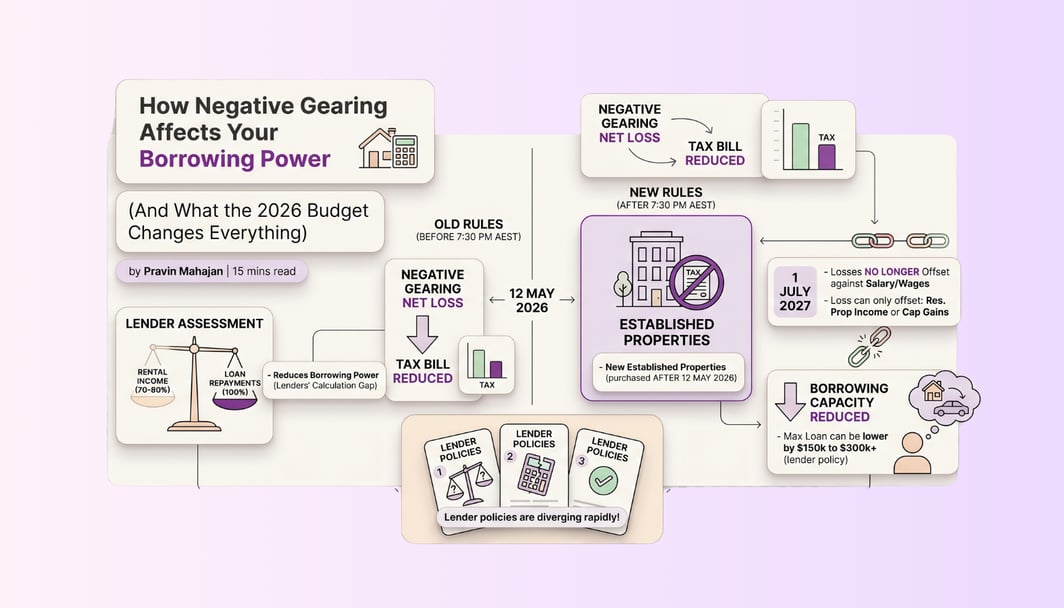

Investors beware: negative gearing is changing the numbers behind investor lending

This is the one that caught a lot of people off guard.

For years, banks factored in the tax refund from negative gearing when they worked out how much you could borrow. It made sense, if you're getting money back from the ATO at tax time, that's real money you can use to service a loan.

But that’s changing now.

The government announced that, from 1 July 2027, negative gearing will apply only to newly built properties. Buy an established home as an investment, and you can no longer use rental losses to reduce your regular tax bill.

Many banks are updating how they assess investor loans to reflect this. The tax refund they used to count on your behalf will no longer be a part of the calculation.

Here's what that means in real numbers. Borrowers who could previously borrow $1 million (for established properties) may suddenly find they now qualify for only around $700,000. That is roughly a 30% reduction in borrowing capacity, even though their personal circumstances have not changed.

MFAA chief executive Anja Pannek said the scale of the Budget means Australians will be seeking clear, practical guidance. "For many people, the question will not be what the Budget means in theory, but what it means for their home loan, their investment property, their business, their cash flow or their future plans," she said.

So how bad is the hit, really?

Here's the honest picture when you stack both changes together:

CBA's economists estimated that the negative gearing change alone is equivalent to your mortgage rate going up by 0.90% to 1.55% in real cash-flow terms. Stack that on top of the three actual rate hikes this year, and you're looking at the functional equivalent of your mortgage rate rising by 1.65% to 2.30% since January, even if only 0.75% has moved on paper.

AMP chief economist Shane Oliver forecast a short-term housing price correction of around 5% as investors recalibrate their after-tax return expectations. "The changes to negative gearing and the CGT discount could result in a 5% or so fall in home prices in the short term as investors retreat," he said.

The changes don’t stop when you buy, selling could cost more too

The budget didn't just change the rules while you hold an investment property. It also changed the rules for selling.

Right now, if you hold a property for more than 12 months, you only pay tax on half the profit when you sell. It's called the 50% Capital Gains Tax discount, and it has been in place since 1999.

From 1 July 2027, that system will be replaced by an inflation-indexation model. Under the proposed rules, the inflation portion of your gain would effectively be excluded, while the remaining “real” gain would be taxed at your full marginal rate (subject to the proposed minimum tax settings). The Budget also introduces a proposed 30% minimum tax on net capital gains. In the past, some investors may have planned to hold onto assets and sell them later in lower-income years, such as retirement, to reduce the amount of tax they paid. The new minimum tax is designed to limit that strategy by ensuring a minimum level of tax still applies to capital gains, regardless of when the asset is sold.

The silver lining is that properties you already own are not immediately affected, although gains accruing after 1 July 2027 may fall under the new rules. That means timing could become an important consideration for investors thinking about selling over the next few years.

What do you mean by inflation indexation?

An inflation indexation model adjusts the purchase price of an asset to account for inflation before calculating tax on any profit.

In simple terms, it tries to separate:

- the part of your gain that simply reflects inflation, and

- the part that represents a “real” increase in value.

Under this type of system, you generally only pay tax on the gain above inflation.

For example:

- You buy a property for $500,000

- Over time, inflation increases prices across the economy by 20%

- Your inflation-adjusted purchase price becomes $600,000

- If you sell the property for $700,000, only the $100,000 gain above inflation may be taxed

This differs from the current Australian CGT discount system, where eligible investors simply receive a 50% discount on the total capital gain after holding the asset for more than 12 months.

What investors should do now?

You're not powerless here. But you do need to act, not wait and see.

- Get your borrowing capacity recalculated, now: Pre-approvals from even six months ago are now out of date. Banks have updated their assessment models. If you're planning to buy an investment property, you need to know what you actually qualify for today, under the new rules.

- Focus on new builds if you want the full tax toolkit: New construction still gets full negative gearing and full CGT discount access. The Budget introduces changes taking effect from 1 July 2027, preserving negative gearing benefits only for new construction. If you're an investor, this is where the tax advantages now live.

- Think about your exit timing on properties you already own: The old CGT rules still apply to gains you realise before 1 July 2027. If you were already thinking about selling, talk to your accountant now about whether selling before that date makes financial sense.

- Stress-test for more rate rises: Some economists are forecasting two more hikes this year. If those happen and you're already at the edge of your borrowing capacity, that's a problem. Factor in a higher interest rate for your calculations when you're making property decisions right now.

- Review your interest-only strategy: Interest-only loans were popular with investors partly because they maximised the deductions you could claim. With those deductions now ring-fenced for established properties, the maths of an IO loan looks different. Worth a conversation with your broker.

What does this mean for the housing market?

The short answer is: it’s complicated, and experts don’t all agree.

If fewer investors buy established properties, house prices in some parts of the market could ease in the short term. But it could also put more pressure on rental supply at a time when Australia is already struggling to build enough homes.

Over time, the changes may push more investors towards new builds, which could help increase housing supply. But that effect is unlikely to happen overnight.

The Budget papers estimate the changes could lead to around 35,000 fewer privately built homes over the next decade. The government says its $2 billion infrastructure fund will help unlock 65,000 new homes instead. Whether that balances out in practice is something the market will determine over time.

For decades, many Australian property investors relied on a common strategy: buy an established property, run it at a loss, and use negative gearing to claim tax deductions while waiting for long-term capital growth.

The death of negative gearing as an investment strategy

However, changes to the financial landscape mean this playbook may no longer work for everyone. Instead, we are seeing a broader shift toward yield-first investing or positive gearing. This strategy focuses on securing strong rental income and immediate cash flow, rather than relying heavily on tax benefits.

This shift may lead investors to consider different options that can support themselves from day one without a tax safety net, such as:

- High-yield regional areas: Property markets outside capital cities that often offer lower entry costs and higher rental yields.

- Rooming houses: Properties leased to multiple tenants on individual contracts to maximise total rent.

- Dual-income properties: Single blocks featuring two separate dwellings, such as a house and a granny flat or a duplex, which generate two rental streams.

- Commercial real estate: Offices, retail spaces, or industrial warehouses, which often provide higher yields and longer leases than residential options.

A positively geared property generates more income than it costs to hold. This means the investment puts money into your pocket each month, rather than requiring you to fund a shortfall out of your own salary. This contrasts with negative gearing, which relies on long-term property value increases to outweigh ongoing losses.

Every investment strategy starts with understanding what you can afford. Before making your next move, it can be helpful to analyse your borrowing power to see how the current rules and interest rates affect your budget.