The RBA cash rate is the interest rate the Reserve Bank of Australia sets for overnight loans between banks. It is Australia's benchmark interest rate and the primary tool the RBA uses to control inflation and keep people employed. The current cash rate is 4.10%, set on 17 March 2026 following a 5–4 Board vote.

When the RBA raises the cash rate, variable-rate mortgage repayments increase. When it cuts, repayments fall. Banks are not required to pass on changes in full and how quickly they move varies by lender. Use Ask Bheja to find out exactly what the current rate means for your loan.

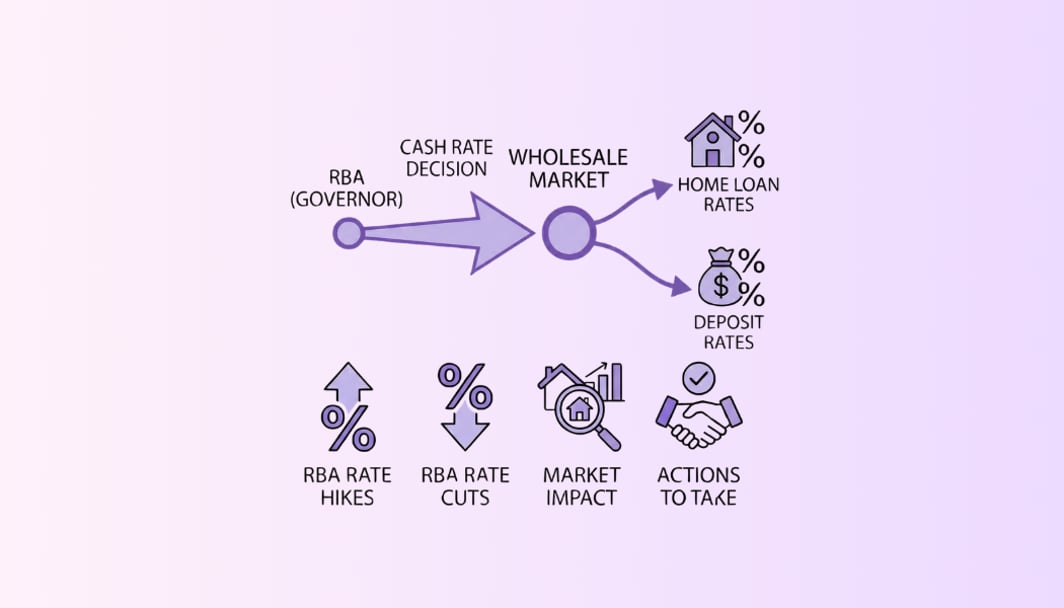

What Is the RBA Cash Rate?

The RBA cash rate is the interest rate banks charge each other for overnight loans. Set by the Reserve Bank of Australia, it acts as the benchmark for all interest rates across the economy from home loans and personal loans to savings accounts and term deposits.

When you take out a variable rate home loan, your interest rate is typically the cash rate plus your lender's margin. With the cash rate at 4.10% and a typical bank margin of 2.00%, your mortgage rate would sit around 6.10%.

The RBA uses the cash rate as its primary monetary policy tool. Raising the rate increases borrowing costs, which slows spending and reduces inflation. Cutting the rate encourages borrowing and stimulates economic activity. Holding it signals the RBA is watching and waiting for more data before acting.

The RBA Board meets eight times per year, roughly every six weeks, to decide whether to adjust the rate.

How Does the RBA Board Decide to Raise, Cut, or Hold the Cash Rate?

The RBA Board consists of nine members: the Governor, the Deputy Governor, the Secretary to the Treasury, and six independent members appointed by the Treasurer. Decisions are made by vote and announced at 2:30 PM Sydney time on the second day of each meeting.

The decision process follows a consistent four-step routine:

Step 1: Before the meeting RBA staff prepare detailed briefings on inflation, employment, GDP growth, global markets, household spending, and financial conditions. These reports are the primary inputs into the Board's deliberations.

Step 2: During the meeting Board members discuss the economic outlook, assess risks on both sides inflation too high vs growth too weak and debate whether the current rate setting is achieving the RBA's dual mandate of price stability and full employment.

Step 3: The decision The Board votes. The outcome raise, cut, or hold is announced at 2:30 PM Sydney time the same day, along with a statement from the Governor explaining the reasoning.

Step 4: After the meeting Detailed minutes are published two weeks later, revealing what was discussed, which risks the Board weighted most heavily, and what data would influence the next decision. These minutes are closely watched by economists, lenders, and mortgage brokers.

The RBA targets CPI inflation between 2% and 3% over time. When inflation sits above this band, the Board leans toward raising or holding rates. When it falls below, rate cuts become more likely.

When Does the RBA Meet in 2026? Full Schedule and Decisions

The RBA Board announces its interest rate decisions at 2:30 PM Sydney time on the following dates:

RBA Cash Rate Meeting Decisions 2025

2025 was the pivot year the RBA delivered three cuts after holding rates at a 12-year high of 4.35% through all of 2024.

What Happens to Your Mortgage When the RBA Raises, Cuts, or Holds?

Every RBA decision flows through to Australian borrowers — but not always immediately, not always in full, and not always equally across all lenders. Here is what each scenario means.

When the RBA Raises the Cash Rate

A rate hike increases borrowing costs across the economy. Variable rate mortgage holders feel it first, banks typically pass on increases within one to two weeks, though the size of the pass-through varies by lender.

On a $600,000 variable rate mortgage, a 0.25% increase adds approximately $90–$95 per month to repayments or around $1,080 per year. Repeated hikes compound: the 13 hikes delivered between May 2022 and November 2023 added over $1,500 per month to the average Australian mortgage.

Fixed rate loans are shielded from hikes until the fixed term expires. But fixed rates often rise in anticipation of future hikes meaning waiting to lock in a fixed rate after a hike announcement may already be too late.

→ See which banks have passed on the latest hike

When the RBA Cuts the Cash Rate

A rate cut lowers borrowing costs but banks don't always pass on the full reduction, and they historically move more slowly on cuts than hikes. During the 2025 cutting cycle, some lenders took up to three weeks to apply cuts to variable rate products.

For borrowers, a cut presents two choices: take the lower repayment and free up cash flow, or maintain current repayments and pay down the loan faster. The second option can save thousands in interest over the life of the loan.

→ Calculate how a rate cut affects your repayments

When the RBA Holds the Cash Rate

A hold decision means the RBA considers the current rate appropriate for economic conditions. It is not a signal that rates will stay on hold forever it means the Board needs more data before its next move.

Importantly, banks can still change their rates during a hold period. Our Open Banking tracker monitors every product across every accredited lender daily a hold from the RBA does not mean your rate is frozen.

→ Check if your bank has moved rates this month

What Does the Current Rate Mean for Your Loan?

Ask Bheja — powered by Open Banking data across every accredited lender in Australia, updated daily.

Try these:

- "How much will my repayments go up on a $750,000 loan at 6.3%?"

- "Has my bank passed on the March 2026 rate hike yet?"

- "Should I fix my rate or stay variable given where rates are heading?"

- "What's the lowest variable rate available in the full market right now?"

- "How much have my repayments increased since the RBA started hiking in 2022?"

How Does the RBA Cash Rate Affect Your Mortgage Rate?

The RBA cash rate is the floor, not the ceiling. Your actual mortgage rate includes your lender's margin on top covering their funding costs, operating expenses, credit risk, and profit. Here is how a 4.10% cash rate typically becomes a 6.10% mortgage rate:

This margin typically 1.50% to 2.50% above the cash rate is why your mortgage rate does not move in perfect lockstep with the RBA. Online lenders and non-bank lenders with lower operating costs often sit closer to the cash rate than the major banks.

Want to see how your bank's current rate compares to the full market? Our Open Banking tracker covers every accredited lender in Australia updated daily. → Compare the full market now

Continue Exploring

Frequently Asked Questions About the RBA Cash Rate

The current RBA cash rate is 4.10%, set on 17 March 2026. The RBA raised it by 0.25% at that meeting following a close 5–4 Board vote, citing persistent domestic inflation and rising global energy prices.