The ABS just dropped February's CPI figures. Headline inflation eased slightly to 3.7%. The commentators are calling it a breather. They're wrong about what it means for your mortgage.

Here's what the headline number is hiding.

The real story inside today's data

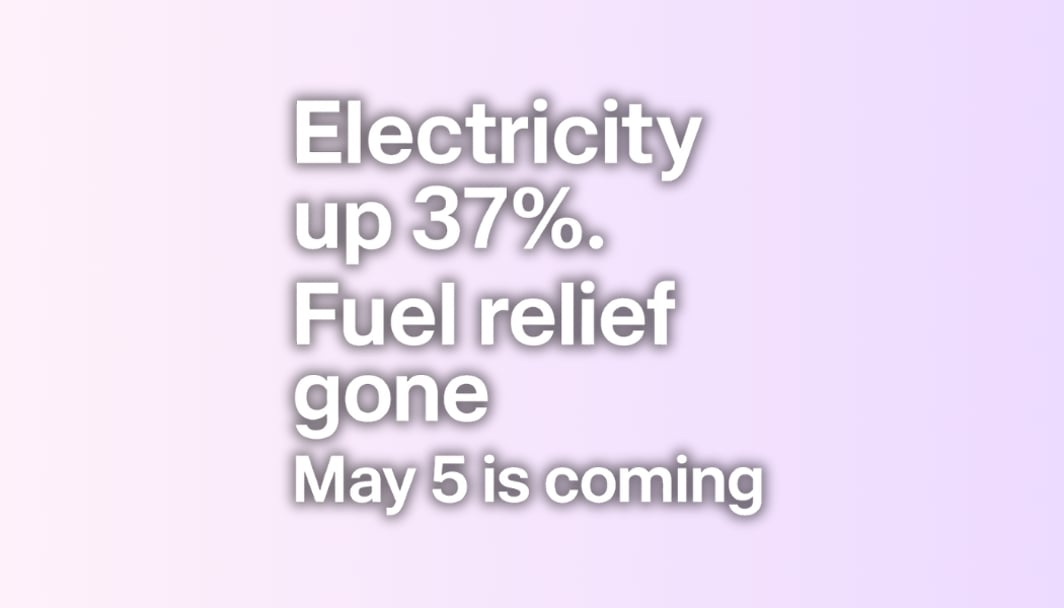

The largest contributor to annual inflation in February was Housing, up 7.2%. Electricity costs alone surged 37% year-on-year, up from 32.2% in January. Australian Bureau of Statistics. That's not a commodity spike. That's structural. The electricity surge is primarily driven by government energy rebates from 2025 being fully used up by households, according to the Australian Bureau of Statistics, meaning that relief is now completely gone, and real energy costs are the new baseline.

Here's the twist that makes this genuinely alarming: excluding the impact of those rebates, electricity prices actually rose just 4.9% in the 12 months to February. Australian Bureau of Statistics. The 37% headline figure is a mathematical artefact of last year's discounts disappearing. That base effect won't reverse. Your bill won't go back down.

The one genuine relief: transport was one of the few categories to provide some relief, falling 0.2% over the year, with automotive fuel prices 7.2% lower than a year earlier, before the Middle East conflict drove oil higher again. Australian Bureau of Statistics

That fuel relief is gone, too, now.

Why "deceptively calm" is exactly right

The February data is already outdated. It was collected before oil prices jumped following the Middle East escalation and before those price rises started showing up at Australian petrol stations and in household energy bills.

What tells the real story right now isn't the ABS data. It's what Australians themselves expect. Consumer inflation expectations have surged to their highest level since mid-2023. People are already bracing for what's coming — and they're usually right.

Westpac's economists have examined the same signals and reached the same conclusion: the March quarter CPI, due April 29, is expected to come in well above the RBA's target. That makes a May 5 rate hike close to a certainty.

The February print isn't approved yet. It's the last quiet moment before a very loud April.

What this means for your loan

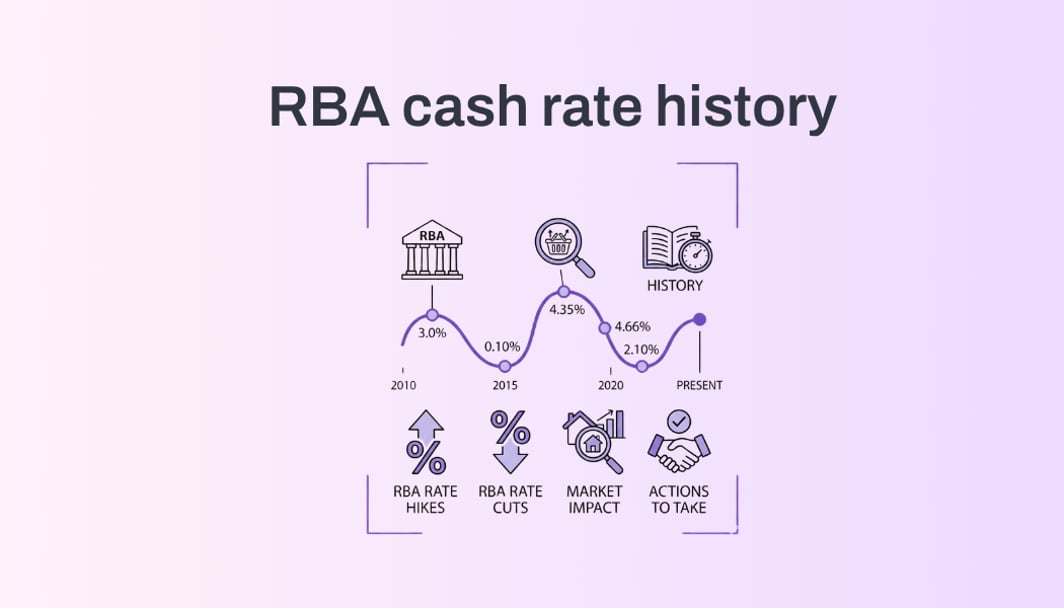

The RBA cash rate is currently at 4.10% after back-to-back hikes. Every major bank is now forecasting a further 25bp increase on May 5. That takes the cash rate to 4.35%, the highest since 2012.

The practical impact on a $600,000 variable mortgage: roughly $90–$100 more per month on top of what you're already paying. And unlike energy rebates, rate hikes don't reverse quickly.

Your 48-hour checklist

Don't wait for May 5. The time to act is before the announcement, not after.

- Call your lender this week. Please mention that you're aware of the May decision and that you're comparing rates. Lenders have more room to negotiate before a hike is public than after. Ask specifically for a reduction in your interest rate margin, not a fixed-rate switch. This is the single most underused lever Australian homeowners have.

- Run the real number. Add 0.50% to your current variable rate (May hike plus potential margin creep). If that repayment squeezes your monthly buffer below $500, you need a plan now.

- Review your energy contract. The 37% electricity surge isn't going to normalise; the rebates that suppressed it are gone. If you're on a default tariff, compare market offers this week. This is money on the table that has nothing to do with the RBA.

- Consider a partial fix, but think it through. Fixing 20–30% of your loan provides cash-flow certainty without locking you out of future flexibility if rates do eventually fall. But check the break costs on your current loan first.

The honest bottom line

The February CPI print is not a green light. It's a snapshot of a world that existed before oil jumped and before the last energy rebate disappeared from every household's bill. The RBA's own forecasts indicate inflation will not return to target until 2028. May 5 is a near-certainty.

Homeowners who act this week will lock in a loyalty discount before their lender has every reason to say no.

The March CPI drops on April 29, 6 days before the RBA decides. We'll break down what it means for your mortgage the same day it lands. Follow us so you don't miss it.