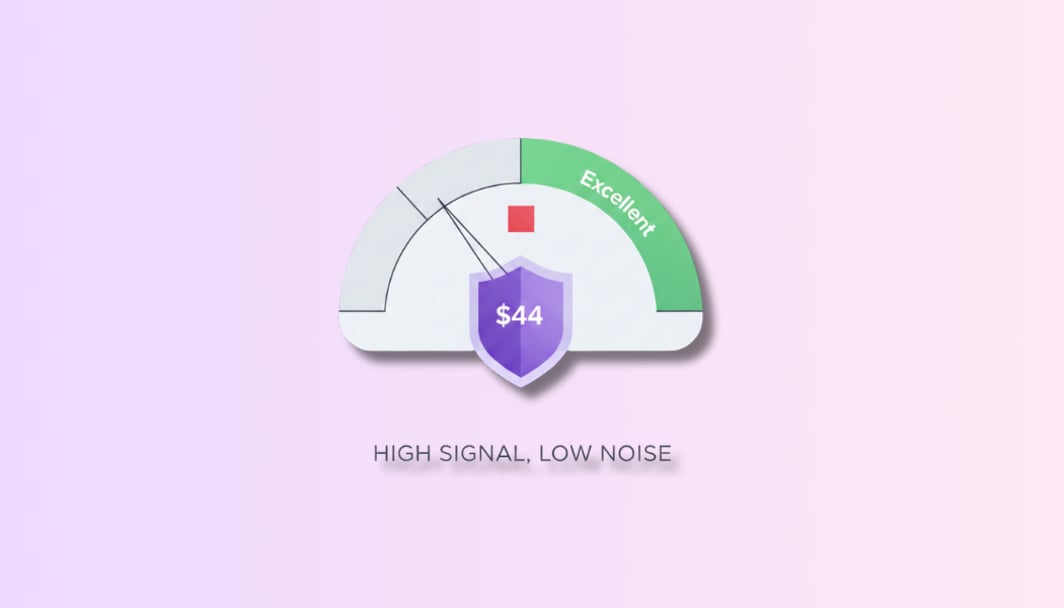

A NSW Supreme Court judge just called a major bank's rate-change emails "at best ambiguous, at worst likely to mislead." A $44 underpayment blocked a borrower from settling on their new home. With Macquarie's rate change effective today, here's what you need to do right now.

NSW Supreme Court — Judgment 16 February 2026

"At best ambiguous, and at worst likely to mislead. The bank's refusal to fix the issue was legally unjustifiable and short on commercial morality."

Justice David Hammerschlag, Chief Judge in Equity — Vinall v Westpac Banking Corporation [2026] NSWSC, Case No. 2026/00030156

$44

Monthly shortfall that triggered an Equifax default report and blocked a property settlement

24

Months a single late-payment marker (RHI) stays on your credit file under Australian law

$0

Minimum dollar threshold for an RHI "late" marker, any amount qualifies for recording

The Case That Changed Everything

📁 Case File: Vinall v Westpac Banking Corporation

The facts are almost absurdly mundane. Following a July 2025 RBA rate cut, St George Bank sent borrower Vinall an automated email notifying them of their new rate. The email , which Justice Hammerschlag would later describe as "at best ambiguous" led Vinall to begin paying the reduced repayment amount one month earlier than the lender required.

The result was a $44 monthly shortfall. Not $440. Not $4,400. Forty-four dollars, less than a tank of petrol.

St George's automated systems flagged the shortfall and reported it to Equifax as a Repayment History Information (RHI) marker. When Vinall attempted to settle on a new property purchase, the marker on their credit file caused their new lender to decline the loan. The settlement collapsed.

"The bank's refusal to rectify the situation was not just legally unjustifiable — Justice Hammerschlag called it 'short on commercial morality.' That phrase will echo through the mortgage industry."

Westpac has been ordered to pay legal costs, and the matter proceeds to the NSW District Court for a full damages assessment, which will likely include the cost of the failed settlement, any bridging finance, and consequential losses.

Australia's peak credit industry body has since called for reform to the reporting regime, with consumer advocates pointing to the case as evidence that the system lacks proportionality for minor, inadvertent errors.

Why the Maths Fails You Every Rate Change

The Vinall case exposed a structural flaw that applies to every Australian mortgage holder, not just St George customers. When a lender sends a "Notice of Variation" email, three separate dates interact, and the gap between them is where defaults are born.

How a rate change becomes a credit file marker

- RBA announces rate decision

Feb 3, 2026. Banks begin calculating new variable rates immediately. - Bank sends "Notice of Variation" email

It states the new rate is "effective" from a certain date. Effective date ≠ first required payment date. - Borrower adjusts repayment,too early or too late

A careful borrower who adjusts immediately can accidentally underpay if the new amount isn't due until the next full billing cycle. - Automated system flags shortfall

Even $1 short triggers an RHI flag. No human reviews it. No warning call. The flag is automatically sent to Equifax. - Credit file shows "1" (late payment)

Stays visible to lenders for 24 months. Tier-1 lenders, often the cheapest, may automatically decline or flag your application.

Understanding RHI vs. Formal Default

Most Australians know about the formal default threshold, $150 overdue for 60 days. Cross that line and a default listing sits on your file for five years. What far fewer people know is that Repayment History Information operates completely separately, with no minimum dollar threshold at all.

Your 24-Hour Checklist

With Macquarie's rate change effective today (20 February) and others still flowing through from the February 3 RBA decision, the window to act is narrow. Do not guess. Do not assume your direct debit has automatically adjusted. Verify each step below.

Action Checklist: Complete Today

1. Log in and verify your exact minimum repayment. Go to your lender's portal right now. Find the field labelled "Minimum Monthly Repayment." Write down the exact dollar amount. Do not calculate it yourself from the new rate. Lenders use slightly different rounding and cycle-timing logic.

2. Apply the $50 Buffer Rule. Set your direct debit to exactly $50 above the new minimum. This single action eliminates virtually all risk of an inadvertent shortfall from rounding errors, timing mismatches, or future micro-adjustments. The overpayment reduces your principal; it is never wasted.

3. Audit your rate-change emails for the specific debit date. Look for the precise wording: "Your new repayment of $[X] will be debited on [Date]." If the email does not include a specific debit date, only an "effective" date, call your lender immediately. Record the name of the representative and the date of your call.

4. Download your free Equifax credit report. Visit equifax.com.au and request your free annual report. Look specifically for any "1" or "2" markers in the Repayment History Information section from January or February 2026. If you find one that is incorrect, dispute it immediately, citing the Vinall v Westpac judgment as precedent.

5. If you find an incorrect marker — act fast. Contact your lender's hardship or credit team directly, not the general customer service team. Put your dispute in writing via email. Reference Case No. 2026/00030156. If the lender does not correct the matter within 30 days, escalate to AFCA (Australian Financial Complaints Authority) at afca.org.au.