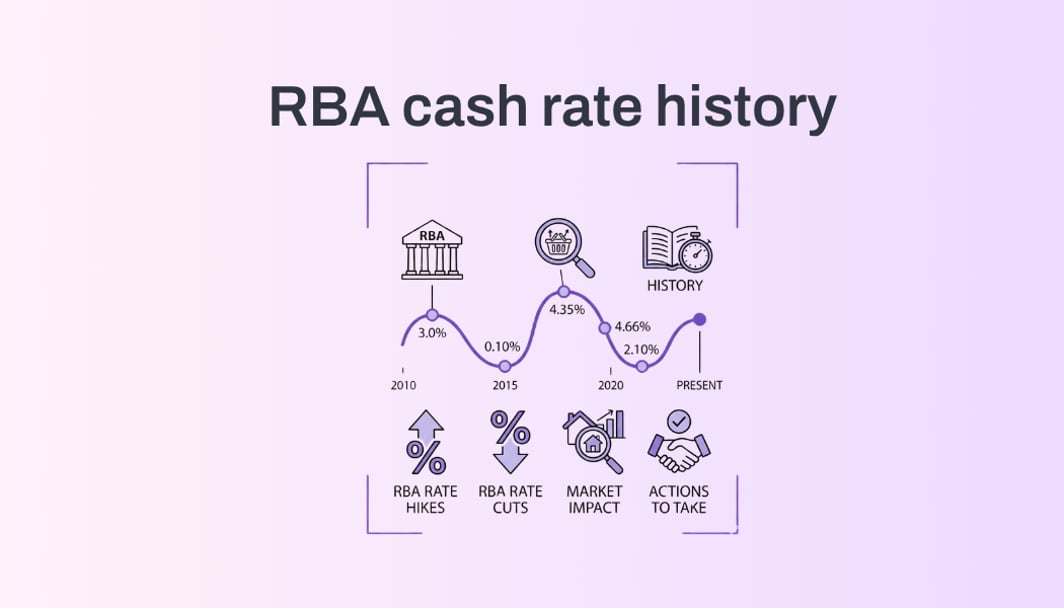

In a move widely expected by markets, the Reserve Bank of Australia has lowered the official cash rate by 25 basis points to 3.85%, at its May meeting.

This is the second rate cut in 2025, as inflation continues to ease and the RBA shifts focus toward supporting household budgets and employment.

"We have got a little more comfortable, just a little more comfortable, that things are going in the right direction, so we can take the foot off the brake just a little bit more,” RBA Governor Michele Bullock said during the post-meeting press conference.

What does the rate cut mean for home loan borrowers?

The Reserve Bank has now delivered its second rate cut for 2025, dropping the cash rate by another 25 basis points to 3.85%. This takes rates back to where they were in May 2023, effectively unwinding nearly a full year of rate hikes.

While the first cut in March gave borrowers a glimpse of relief, this second move adds real weight. It not only compounds savings but also reduces the pressure on household budgets that have been under strain from rising mortgage costs, high insurance premiums and energy bills.

For borrowers on variable rates, this decision can translate into meaningful savings — but only if your lender passes the cut on.

The good news: All Big Four banks — Commonwealth Bank, Westpac, NAB and ANZ — have already announced they’ll pass on the full 0.25 percentage point reduction to their variable rate home loan customers. Depending on your bank, the lower rate will kick in between May 30 and June 3.

Some smaller banks and non-bank lenders have also followed suit, but others may be slower to respond or pass on only part of the cut. Borrowers should watch their lender’s announcements closely, because how much you save depends on whether your rate actually comes down — and by how much.

How much can you potentially save on your home loan after the cash rate cut?

With the RBA cutting the cash rate by another 0.25%, many borrowers are now wondering what this actually means for their home loan.

On Bheja, you can get a quick, personalised view of your savings in seconds. Just enter your loan amount, interest rate, and term — and Bheja will break it down for you instantly.

Here’s one example:

A borrower with a $1.1 million loan, 30-year term, and a variable rate of 6.24%, could now see their rate drop to 5.99%, once the full cut is passed on.

Here’s how that plays out:

That’s over $2,100 in yearly savings, or enough to cover your rising insurance premiums or offset grocery bills.

More importantly, it shows just how much even a small rate cut can reduce your long-term costs.

💡 Pro tip: If your budget allows, consider keeping your monthly repayments the same as before. That way, you chip away at your loan faster and save more in the long run.

See your savings from the latest rate cut

Choose a loan size and term to see how the latest cash rate change affects you.

What should you do next?

The second RBA rate cut of 2025 is now in motion. If you’ve got a variable rate home loan, here’s how to make sure you benefit from it — and don’t leave savings on the table.

✅ 1. Check if your lender is passing it on

The Big Four banks — CBA, NAB, Westpac and ANZ — have already confirmed they’ll pass on the full 0.25% cut. Depending on your bank, the new rate will kick in between May 30 and June 3.

Other lenders may move slower or not pass on the full cut. Check your lender’s announcement or your next mortgage statement to confirm.

✅ 2. Don’t just accept your new rate — compare it

Your rate may drop, but that doesn’t mean it’s competitive. A small difference in your home loan interest rate could save you thousands per year. If your lender’s new rate still feels high, it may be time to consider refinancing.

👉 On Bheja, you can instantly compare personalised rates based on your loan amount — no guesswork.

✅ 3. Keep repayments steady (if you can)

Even if your new repayment is lower, consider sticking to your old amount. Doing this means more of your payment goes to the principal — which helps pay off your loan faster and cuts down your total interest bill.

✅ 4. Re-check your rate regularly

Rates are on the move, and more cuts may come later this year. With Bheja, you can easily re-check your rate anytime and stay ahead of the curve.

Bheja puts you in control!

Whether you want to lower repayments, pay off your mortgage faster, or just make sure you're not overpaying, Bheja’s mortgage health check makes it easy, fast, and stress-free.