Key Takeaways

- A honeymoon rate (also called an introductory rate) is a discounted interest rate offered by lenders for the first 1 to 2 years of a home loan.

- When the honeymoon period ends, your loan automatically rolls onto a higher "revert rate", often significantly above the market average.

- In 2026, with variable rates sitting between 6.0% and 6.5%, the revert rate on some introductory products is landing borrowers on rates above 7%.

- The strategy that works: use the lower repayments during the honeymoon period to get ahead on your loan, then refinance before the revert rate kicks in.

- Always compare the revert rate, not just the honeymoon rate, when evaluating these products.

What is a Honeymoon Rate?

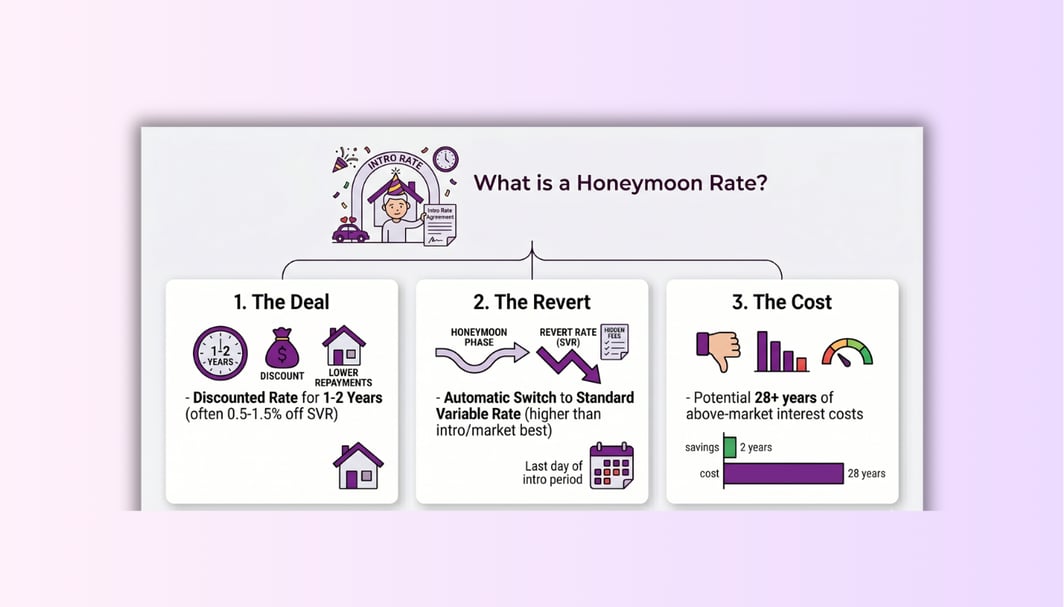

A honeymoon rate is a temporarily discounted interest rate that a lender offers new borrowers at the start of a home loan. It is designed to make the loan appear attractive and to help borrowers manage repayments during the financially demanding early years of homeownership.

The "honeymoon" typically lasts between six months and two years. After that period, the rate reverts to the lender's standard variable rate. That standard rate is almost always higher, sometimes considerably higher, than both the introductory rate and the best rates available elsewhere on the market.

Honeymoon rates are also called introductory rates, intro rates, or discounted variable rates. They are the same product with different names depending on the lender.

How does a honeymoon rate work?

Here is the mechanics of a honeymoon rate loan in plain terms:

Phase 1: The honeymoon period (typically 1 to 2 years) Your interest rate is set at a discounted level, often 0.5% to 1.5% below the lender's standard variable rate, making your repayments lower than they would be on a standard loan. This is genuinely useful, it eases cash flow when you are also paying stamp duty, legal fees, moving costs and furnishing a new home.

Phase 2: The revert (the part lenders do not advertise loudly) When the honeymoon period ends, your loan automatically switches to the lender's revert rate. You do not need to do anything. It happens without a letter, without a phone call, and often without any reminder at all.

The revert rate is the lender's standard variable rate, which is rarely their most competitive product. It is the default rate that borrowers end up on when they are not actively shopping, and it is how lenders recoup the margin they gave up during the honeymoon period.

The result: many borrowers save money for 12 to 24 months, then spend the remaining 28 years of their loan paying above-market interest without realising it.

Honeymoon Rate vs Revert Rate: A worked example

Here is how the numbers play out on a typical Australian home loan in 2026.

Loan details:

- Loan amount: $650,000

- Loan term: 30 years

- Honeymoon rate: 5.49% (1-year introductory period)

- Revert rate: 7.10% (lender's standard variable rate after honeymoon ends)

- Comparable market rate: 6.15% (competitive variable rate available elsewhere)

The honeymoon saving: $660 per month vs the revert rate during year 1 ($7,920 over the year).

The revert rate cost: $390 per month more than the best available market rate, every month for the remaining 29 years. That is $135,720 in extra interest over the life of the loan if you never refinance.

This is why experienced borrowers and brokers treat honeymoon rates with caution. The saving during the introductory period is real but short-lived. The cost after it ends is much larger and lasts much longer.

Why do lenders offer honeymoon rates?

Honeymoon rates are not a gift. They are a customer acquisition strategy.

Lenders know that most borrowers, once they are set up with a lender and have a direct debit running, are unlikely to refinance. The administrative effort of switching, gathering documents, getting a new valuation, going through the application process, is enough to keep the majority of borrowers in place even when better rates are clearly available.

This is sometimes called the loyalty tax: existing customers consistently pay more than new customers, and lenders rely on that inertia.

The honeymoon rate gets you in the door. The revert rate is where the lender makes its margin. The model works because most borrowers do not monitor their rate after settlement.

There is also an ASIC-regulated disclosure requirement at work. Lenders must show a comparison rate alongside every advertised rate. The comparison rate takes into account fees and the average cost of the loan over 25 years, which means a high revert rate drags the comparison rate well above the honeymoon rate. This is worth checking before you sign.

Are honeymoon rate loans still available in 2026?

Yes, though they are less common than they were in the early 2000s when they proliferated across the market.

True introductory rate products, where the rate is set below the lender's standard variable for a set period, are offered by a smaller number of lenders today. Many lenders have moved to a different model: offering a discounted variable rate that tracks the market throughout the loan term rather than reverting to a penalty rate.

What has replaced the traditional honeymoon rate in many cases is the cashback refinance offer. Rather than a lower rate upfront, lenders offer $2,000 to $4,000 cash on settlement, then apply a competitive market rate from day one. For many borrowers, this is a better deal than a discounted rate that reverts after 12 months.

The core principle, however, remains the same: lenders use short-term incentives to acquire customers they hope will stay for decades. Whether the incentive is a honeymoon rate or a cashback, the question to ask is always: what does this loan cost me in year 3, year 5, and year 10?

Honeymoon Rate vs Fixed Rate: What is the difference?

A common point of confusion. Both involve a lower rate for an initial period, but they work differently.

The key distinction: during a honeymoon period, your rate is still variable and can move with RBA cash rate changes. During a fixed rate period, your rate does not move regardless of what the RBA does.

Both products carry a revert rate risk at the end of their initial period. The strategy for managing both is the same: refinance before the revert rate activates.

Five things to check before taking a honeymoon rate

1. What is the revert rate?

Ask the lender directly: what exact rate will this loan roll to after the introductory period ends? Get it in writing. A honeymoon rate of 5.49% that reverts to 7.10% is a very different product to one that reverts to 6.20%.

2. What is the comparison rate?

The comparison rate is calculated over the full loan term and reflects the true average annual cost including the revert rate. If the comparison rate is substantially higher than the honeymoon rate, that gap tells you how punishing the revert rate is. A comparison rate of 7.50% on a honeymoon rate of 5.49% is a very loud warning sign.

3. Are there exit fees or switching fees?

Some honeymoon rate products include a fee if you refinance within a set period. This fee is designed to keep you on the revert rate even once you realise it is uncompetitive. Check the loan contract specifically for deferred establishment fees, early exit fees, or clawback provisions.

4. Can you make extra repayments during the honeymoon period?

One legitimate use of a honeymoon rate: making extra repayments during the low-rate period to reduce your principal faster before the revert rate kicks in. Some products restrict extra repayments or charge fees for them. If you plan to use the honeymoon period to get ahead, confirm this is permitted before signing.

5. What is the equivalent non-honeymoon product?

Ask your broker to show you the same lender's standard variable product alongside the honeymoon rate product. Run the total interest payable over 5 years across both. In many cases, the standard variable product with a lower revert rate will cost less in total even though the year-one repayments are higher.

The Smart Strategy: use the honeymoon, escape the revert

There is a way to benefit from a honeymoon rate without getting caught by the revert rate, but it requires discipline and planning from day one.

Step 1: Set a refinancing reminder before you sign On settlement day, add a calendar reminder for three months before your honeymoon period ends. That is your window to start the refinancing process. Refinancing takes 4 to 8 weeks from application to settlement, so three months gives you enough buffer.

Step 2: Use the lower repayments to build equity During the honeymoon period, consider making extra repayments rather than reducing your monthly payment to the minimum. Every extra dollar you pay down reduces your loan-to-value ratio (LVR) and makes you more attractive to a new lender when you refinance.

Step 3: Start comparing before the honeymoon ends Do not wait until the revert rate activates. By that point you have already paid one or two months of above-market interest and your motivation to refinance may have faded. Start comparing three months before the honeymoon ends while the urgency is fresh.

Step 4: Do not take the loyalty discount as a substitute for refinancing Some lenders, knowing their customers are about to refinance, will offer a retention discount when you call to leave. This is usually better than the revert rate but still not as good as the best available market rate. Use it as a negotiating tool, not as a reason to stay.

How does the honeymoon rate relate to the "Loyalty Tax"?

The loyalty tax is a term coined by the RBA to describe the pattern of existing borrowers paying consistently higher rates than new borrowers. RBA research found that on average, existing borrowers pay around 0.5 percentage points more than new customers on equivalent loan products.

Honeymoon rate loans are a specific version of this dynamic. The lender prices new customers aggressively for 12 to 24 months, then relies on inertia to keep them at a higher rate for the remaining 28+ years of the loan.

The loyalty tax is not unique to honeymoon rate products. It applies across most variable rate products, but it is most extreme on introductory rate loans because the gap between the introductory rate and the revert rate is deliberately engineered to be large.

Frequently Asked Questions

How Bheja.ai Can Help

Comparing a honeymoon rate loan to a standard variable rate product requires running total interest calculations over a 5 to 10 year horizon, not just looking at year-one repayments. Bheja.ai's comparison engine does this automatically across more than 100 lenders, showing you the true total cost of each product including fees and the revert rate.

If your honeymoon period is ending soon, our home loan health check can show you what rate you should be on compared to what you are on, and which lenders on our panel have competitive products available for your LVR and income profile.

Compare home loan rates across 100+ lenders

Run a free home loan health check

Use our refinance calculator Ask Bheja about your options

This article provides general information only. It does not constitute financial advice. Bheja Group Pty Ltd (ABN 31683827938) is a Corporate Credit Representative (CR 570637) of Purple Circle Financial Services Pty Ltd (ACL 486112). Always seek independent financial advice before making borrowing decisions.