There's a moment most parents miss.

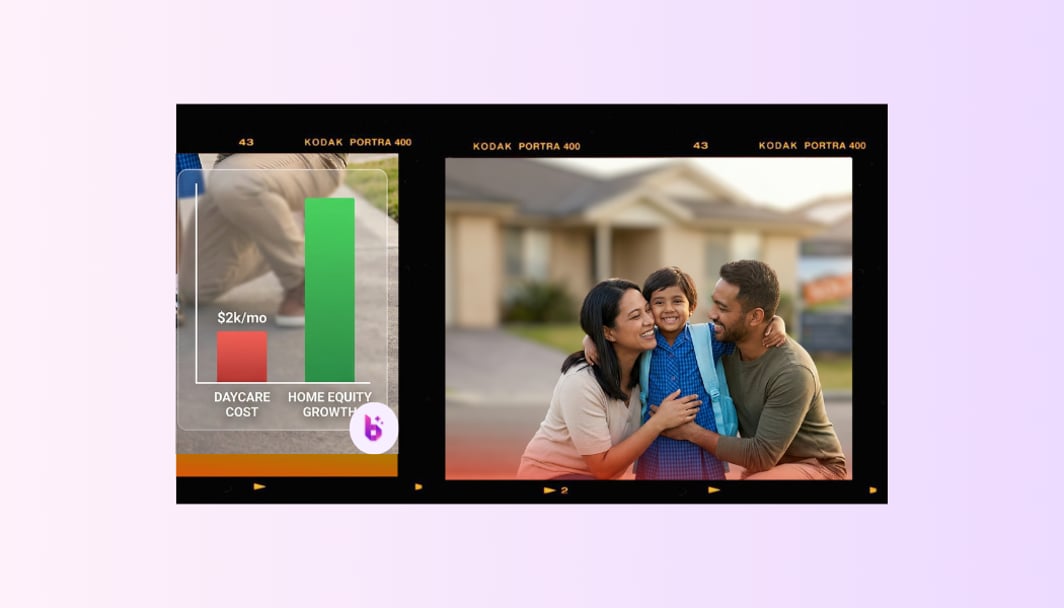

Their youngest finishes their last day of daycare. There are photos. Maybe some tears. And then, quietly, without fanfare, $2,000 a month stops being withdrawn from the family bank account.

That's $24,000 a year.

The Daycare Dividend refers to the monthly cash flow surplus that Australian families gain when their child moves from full-time long day care to a public primary school.

With average childcare costs running at $160–$180 per day, most families free up between $1,500 and $2,000 per month at this transition point.

When redirected immediately into a mortgage offset account, this surplus can reduce a standard 22-year loan by over a decade and save approximately $342,000 in interest.

There's a moment most parents miss.

Their youngest finishes their last day of daycare. There are photos. Maybe some tears. And then, quietly and without any big announcement, $2,000 a month stops leaving the family bank account.

That's $24,000 a year.

Most families don't notice it as a lump sum. It arrives as slightly less stress at the end of the month. A holiday that didn't feel quite so guilty. A car upgrade. A new couch.

The bank notices, though. Your regular repayments tick along unchanged, and the extra cash flows into your spending life without touching your mortgage.

That's the Daycare Dividend, but most Australians end up leaving it with the bank without realising.

What $2,000 a month actually does to your mortgage

Redirecting $2,000 a month in extra repayments onto a typical Australian home loan isn't a nice-to-have financial move. It's a decade-changing one.

On a $700,000 loan with 20 to 25 years left, putting an extra $2,000 a month toward your repayments could cut 7 to 10 years off your loan. That’s not just time saved; it could also mean saving hundreds of thousands of dollars in interest you might otherwise pay.

The maths works because of how interest compounds. Your minimum repayments are set up so you pay for the full loan term. Every dollar you pay above the minimum goes straight to the principal, which then reduces the interest charged on future payments. The effect isn’t a straight line. The sooner you start, the more you save.

This isn’t about refinancing. You don’t need a new rate or a new lender. You just need to make one decision: ask the bank to keep less of your money.

The inertia trap

The Daycare Dividend only works if you intentionally redirect it. The financial system is not going to do that for you.

When childcare costs drop off, lifestyle absorbs the gap. A larger grocery bill here. A weekend away there. Streaming subscriptions you'd been quietly putting off. None of it is reckless. It's just human.

But consider what's on the other side of the ledger.

Your bank has collected years of your loyalty, your on-time repayments, your steady balance, and your tendency to stick with the same routine. They aren’t hoping you’ll pay off your loan faster. The longer your loan lasts, the more interest they earn.

The system benefits when you do nothing. The Daycare Dividend is yours only if you choose to take it.

Three ways to put it to work

1. Extra repayments directly onto the loan

Most variable-rate home loans allow unlimited extra repayments at no cost. Increase your regular repayment by $2,000 a month, or set up a standing transfer of that amount into the loan.

Check if your loan allows this. Most variable loans do, but fixed rate loans often have yearly limits, so plan to do this when your fixed term ends.

2. Redirect it into an offset account

An offset account is a linked account that reduces the interest charged on your mortgage. Every dollar sitting in an offset effectively earns the equivalent of your mortgage interest rate, tax-free. That's a hard return to beat in most savings accounts, and it gives you the flexibility to access the funds if you need them.

3. Run the maths on your specific loan first

Before you decide, use Bheja's Extra Repayments Calculator to model what redirecting $2,000 a month would actually do to your balance, term, and total interest. The number may surprise you.

A word on rate

This calculation assumes your current rate is competitive.

Many Australian families are still on a rate that made sense three years ago and has quietly drifted into overpayment territory. If your home loan hasn't been reviewed since before the rate cycle started, there's a real chance you're already paying more than you should be.

If your rate isn’t right, the order is important: fix your rate first, then redirect the extra money. Having a lower rate and adding $2,000 a month in extra repayments is the strongest way to use this strategy. Health Check through Bheja takes five minutes and tells you exactly where you stand: whether your rate is competitive, what restructuring your repayments could achieve, and what options are available across 100+ lenders.

The moment is now

The daycare years are exhausting. They're also expensive. When they end, there's a very human temptation to breathe out, relax, and quietly absorb the extra cash into a more comfortable life.

But there’s another way to use this moment. If you choose to redirect the $2,000, you could find yourself mortgage-free ten years sooner. Less debt. More choices. A different kind of freedom.

You just got a $24,000/year raise. Don't let the bank keep it.

Run your free Loan Health Check.