How APRA's New Debt-to-Income Restrictions Are Reshaping Australian Home Lending

Key Takeaways

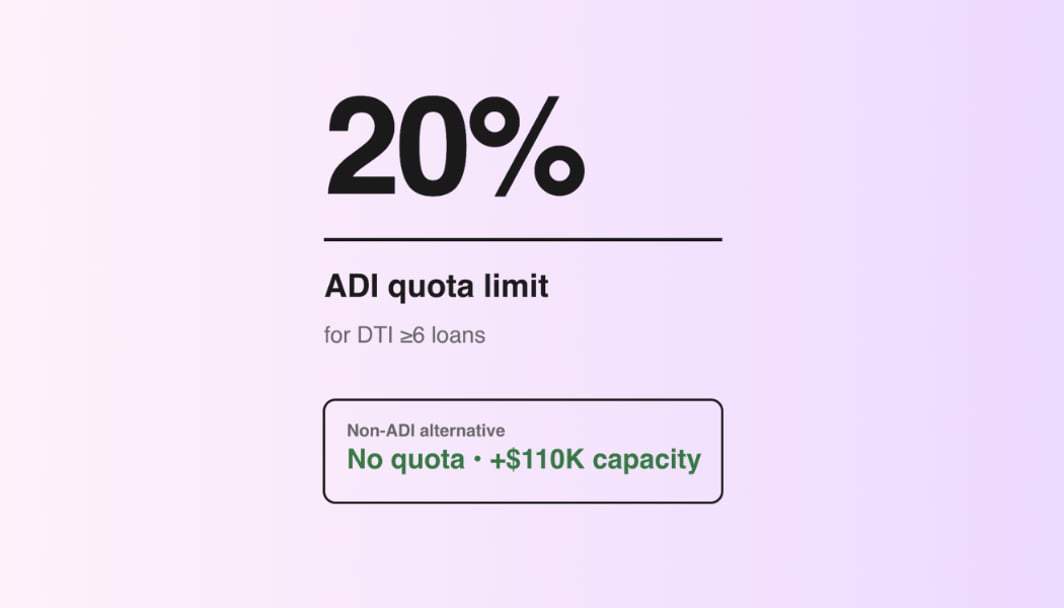

- APRA now limits ADI banks to 20% of new loans with DTI ≥6 (effective February 1, 2026)

- Non-ADI lenders face no DTI quota restrictions and can approve high-DTI borrowers freely

- Switching from ADI to Non-ADI can unlock $80,000-$110,000 in additional borrowing power

- Trade-off: Non-ADI rates are typically 0.25%-0.50% higher than major banks

As of February 1, 2026, APRA's new Debt-to-Income (DTI) restrictions have fundamentally changed how Australian banks approve home loans. If your DTI ratio is above 6, you're now competing for just 20% of available loan slots at major banks, but there's a legal workaround most borrowers don't know about.

Why This Matters Right Now: Major banks have already begun declining borrowers they would have approved 90 days ago. By Q2 2025, industry sources predict the 20% quota will tighten further as property demand remains strong and banks prioritise their quota for high-value clients. The window to secure pre-approval under current conditions is closing rapidly.

What is the APRA DTI Limit? (Update)

The Australian Prudential Regulation Authority (APRA) has implemented a hard cap requiring all ADI-regulated lenders (major banks, credit unions, building societies) to limit high-DTI lending to 20% of their total new residential mortgage lending.

What this means in practice:

- If you're applying for a loan with a DTI ratio of 6.0 or higher, you're now in a restricted category

- Banks must carefully ration these high-DTI approvals across each quarter

- Once a bank reaches its 20% quota, high-DTI applications face either outright decline or significant rate premiums

- This quota resets quarterly, creating a cycle of availability and scarcity

The critical point: Non-ADI lenders are not subject to this restriction. They can approve DTI ratios of 6.5, 7.0, or even higher without quota concerns, provided the borrower meets serviceability requirements. We wrote about it since the announcement Quite Cap.

ADI vs Non-ADI Lenders: The Critical Difference

Understanding the fundamental difference between these two lender types is essential for navigating the new lending landscape. The distinction isn't just regulatory—it affects pricing, approval odds, and your entire borrowing strategy.

ADI Lenders: The Traditional Banks

Who they are:

Commonwealth Bank, Westpac, ANZ, NAB, Macquarie Bank, and most credit unions and building societies.

How they're funded:

ADIs (Authorised Deposit-taking Institutions) use customer deposits, your savings accounts, term deposits, and transaction accounts, to fund their lending. This is why they're heavily regulated.

The regulator:

APRA (Australian Prudential Regulation Authority) oversees their operations with strict lending standards to protect depositors.

The DTI constraint:

Maximum 20% of new loans can have DTI ≥6. This is a hard regulatory ceiling that cannot be exceeded.

The behavioural impact:

When a major bank approaches its quarterly quota, they implement several strategies:

- Adding rate premiums (typically 0.30%-0.50%)

- Requiring larger deposits

- Declining applications despite strong serviceability

- Reserving quota slots for high-value customers (private banking clients, existing customers with substantial deposits)

Non-ADI Lenders: The Alternative Path

Who they are

Specialist lenders including Firstmac, Pepper Money, Liberty Financial, Resimac, La Trobe Financial, and others.

How they're funded:

Non-ADIs don't accept customer deposits. Instead, they raise capital through wholesale funding markets, selling mortgage-backed securities to institutional investors, obtaining warehouse facilities from major banks, or accessing capital markets directly.

The regulator:

ASIC (Australian Securities and Investments Commission) regulates their conduct under responsible lending obligations, but they are not subject to APRA's prudential standards.

The DTI approach:

No regulatory quota on high-DTI lending. Their limit is determined by investor appetite and their own risk models. Many routinely approve DTI ratios of 6.5 to 7.5 for high-quality borrowers.

The flexibility advantage Non-ADIs typically use:

- Lower serviceability buffers (1.0%-2.0% vs. 3.0% for banks)

- More generous income treatment (often accepting 90%-100% of rental income vs. 80% at banks)

- Case-by-case assessment rather than automated policy overlays

The Serviceability Mathematics: ADI vs Non-ADI

The real difference emerges in how each lender type assesses your ability to service a loan. While both must meet responsible lending obligations, their methodologies differ significantly.

The Buffer Advantage: Real Numbers

The serviceability buffer is where Non-ADI lenders create the most dramatic advantage. Here's how it works for a borrower earning $150,000 annually:

ADI Bank Calculation:

- Current interest rate: 6.20%

- Assessment rate: 6.20% + 3.0% buffer = 9.20%

- Maximum borrowing capacity: approximately $720,000

Non-ADI Calculation:

- Current interest rate: 6.55%

- Assessment rate: 6.55% + 1.5% buffer = 8.05%

- Maximum borrowing capacity: approximately $830,000

Result: $110,000 additional borrowing capacity

This increased capacity can be the difference between securing your target property or being outbid. In markets where property prices are rising 0.5% to 0.8% monthly, waiting months for bank quota availability could cost more than years of slightly higher interest payments.

Your 3-Step Action Plan for High DTI Approval

If your DTI is currently 5.8 or higher, you're in the danger zone for bank quota restrictions. Here's your strategic playbook:

Step 1: Calculate Your Exact DTI (Today)

Use the formula above to determine your precise DTI ratio. Be comprehensive in your calculation:

- Include ALL credit facilities (even if unused)

- Multiply total credit card limits by 5

- Use gross income (before-tax)

- Include car loans, personal loans, and HECS/HELP debt

Quick optimisation: If you're close to the 6.0 threshold (say, 6.1 to 6.3), immediately cancel unused credit cards and store cards. Each $10,000 in credit limits you cancel removes $50,000 from your DTI debt calculation.

Step 2: The Critical Quota Check

If working with a mortgage broker, ask them explicitly:

"Which ADI lenders on your panel currently have availability in their 20% high-DTI quota for this quarter?"

If the answer is "None," "It's very tight," or "Only for existing customers," you should pivot immediately to Non-ADI options rather than wasting time on applications likely to be declined.

Important timing consideration: Quotas reset quarterly (January 1, April 1, July 1, October 1). The first 4-6 weeks of each quarter typically have the most quota availability. By week 10-12, major banks are often rationing heavily.

Step 3: Accept the Strategic Trade-Off

If your DTI is ≥6.0 and bank quota availability is limited, seriously consider the Non-ADI path. Here's the honest cost-benefit analysis:

The Cost:

- Interest rates typically 0.25% to 0.50% higher than major banks

- Potentially fewer features (some Non-ADIs lack offset accounts or have limited redraw)

- Possibly higher ongoing fees

The Benefit:

- Approval certainty: no quota games

- Higher borrowing capacity ($80,000-$110,000 more on $150,000 income)

- Faster settlement (often 25-30 days vs. 45+ days with major banks)

- Ability to secure property in rising markets without delay

The mathematics: On a $900,000 loan, a 0.35% rate difference costs approximately $3,150 annually. If property prices in your target market are rising 0.5% monthly, waiting 3 months for bank quota availability could cost you $15,000+ in price appreciation on a $1,000,000 property. The rate premium pays for itself if it allows you to secure the property now.

Refinance strategy: Many borrowers use Non-ADI lenders to secure the property, then refinance to a major bank after 12-24 months when their DTI has improved (through pay rises, debt reduction, or property value growth increasing their equity position).

Frequently Asked Questions

Yes. While Non-ADI lenders don't hold APRA licenses, they are regulated by ASIC and must comply with the National Consumer Credit Protection Act. Established Non-ADI lenders like Firstmac, Pepper Money, and Liberty have operated for decades, managing billions in loan assets. Your loan contract is legally enforceable and your property rights are protected under Australian law regardless of lender type.

Important Risk Disclosures

While Non-ADI lenders offer valuable flexibility, borrowers should carefully consider:

Responsible borrowing principle: Just because a lender will approve a certain amount doesn't mean you should borrow it. Consider your genuine repayment capacity, lifestyle needs, and future plans before maximising your borrowing power.

Next Steps: Act Now

Time sensitivity: Property prices in Sydney and Melbourne rose 0.8% in January 2025 alone. Brisbane is up 1.1%. Waiting 60-90 days for bank quota availability could cost significantly more than accepting a slightly higher rate today.

Your action checklist:

- Calculate your DTI using the formula in this article (today, not tomorrow)

- Cancel unused credit cards and store cards immediately if you're near the 6.0 threshold

- Contact a mortgage broker who works with both ADI and Non-ADI panels (not all brokers have access to Non-ADI lenders)

- Ask explicitly: "What is the current high-DTI quota availability at major banks, and which Non-ADI lenders can you access?"

- If quota is tight or unavailable, request simultaneous pre-approval from both ADI and Non-ADI lenders to maximise options

- Review full costs over 2-3 years, not just headline interest rates, when comparing offers

Final Thought

The DTI quota system has created a two-tier lending market in Australia. Borrowers with DTI ratios below 6.0 enjoy the traditional competitive banking environment. Those above 6.0 must navigate a constrained quota system at major banks or embrace the Non-ADI alternative.

The good news: understanding this system gives you strategic advantage. While others are being declined without understanding why, you can proactively choose the right lending path for your circumstances and act decisively.

The difference between securing your property and missing out often comes down to knowledge and timing. You now have the knowledge. The timing is up to you.